In a recent speech, the head of the main government workers union in the United States accused the Reagan administration of “bleeding” the nation in order to finance defense spending and tax breaks for the rich. It is now clear that one cherished national social institution which is scheduled by the Reagan crowd for a major blood-letting is the Social Security System.

It is surely a symptom of the present government’s financial and political desperation that this hallowed sector of our wobbly welfare state should come under a slashing attack from the Reagan crowd. For more than forty years the contributors and beneficiaries of the Social Security System (there are, at the present time, 116 million enrolled people eligible to contribute via payroll taxes and 36 million cash-benefit recipients) have had it drummed into their heads, for reasons of high policy which we shall explain later, that the benefits promised by the system are sacrosanct. Over and over, year after year, they have been assured that they are legally, equitably, and morally entitled to the benefits promised under the Social Security law without a means test of any kind. According to these assurances, the basis of the entitlement is that the principal benefits, the monthly cash benefits for age and disability retirees and their dependents, the monthly cash benefits for dependents of deceased workers, and the hospital benefit part of Medicare, are all of them required to be paid exclusively out of funds flowing in from payroll taxes and from the special Social Security earned income tax contributions of the self-employed. (The latter are very similar to payroll taxes and we shall, for convenience, include them in that category.)

The Social Security setup requires that the payroll taxes designed for the financial support of the system be adjusted from time to time so that the sum total of the money flowing in from these taxes will, over the long term, be large enough to cover the money flowing out to the system’s beneficiaries. A pay-as-you-go, cash-in/cash-out system is contemplated with only small reserves which are intended to fluctuate up and down in exactly the same fashion as the social insurance systems of many other nations around the world. The Social Security payroll tax inflow is allocated to three different trust funds: the Old Age and Survivors Insurance Trust Fund, the Disability Insurance Trust Fund, and the Hospital Insurance Trust Fund. The benefit outflow, of course, comes out of those same funds.

It is recognized that, as with any pay-as-you-go system, the payroll tax inflow and the cash benefit outflow cannot be exactly matched for each individual calendar year. If that happened the Trust Funds would always have zero balances. Some years the tax inflow will be larger, some years the benefits outflow will be larger. For this reason it is desirable to set the Social Security payroll-tax rates high enough so that in most years, hopefully years of economic prosperity, the tax inflow will exceed the benefit outflow by a small margin. These margins or differences between inflow and outflow are meant to be accumulated, invested, and to earn interest. In total these accumulated differences, or asset balances, serve as an informal economic or contingency reserve.

The trust fund asset balances, or reserves, that we have just described, are meant to be utilized or drawn down or paid out-all these words mean the same thing-during depressions or recessions when the individual years’ benefit outflows would naturally exceed inflows because of the impact of unemployment and early retirement. For unemployment reduces the Social Security tax inflow, since the unemployed don’t produce payroll taxes, while the early retirement of unemployed workers swells the cash benefit outflow.

In recent years a new and unexpected factor has come into further disturb the year-by-year balance between tax inflow and benefit outflow. Consumer prices have been increasing faster than wages; real wages have been falling (most economists believe that this situation will last, at most, a few years). Now since Social Security monthly cash benefits are indexed to the CPI (Consumer Price Index of the U.S. Department of Labor), this means that benefit outflow is, for the time being, increasing more rapidly than the wages on which Social Security taxes are paid. Hence it also means that the benefit outflow is increasing more rapidly than the Social Security payroll-tax inflow and that the asset balances in the trust funds are going down. This trust fund asset decline is a problem of a very temporary character which, as we shall show later, is not difficult to handle. Rising and falling asset balances are a normal feature of any pay-as-you-go system. However they furnish many openings for the enemies of Social Security to exaggerate, distort, and misrepresent any temporary financial difficulties that the system experiences.

At this point we wish to explain more fully the logic of Social Security entitlements. The principle which is most often cited as the foundation of the Social Security System is that benefit payments must be narrowly confined and limited to the levels permitted by the yield of the various Social Security payroll taxes. This form of limitation is a purely American phenomenon, and American workers have been literally brainwashed to believe in this principle as if it were Gospel Truth. The fact is that practically every other national social-security system in the world provides money for benefits from general revenues of the government in addition to payroll tax income which is directly earmarked for the Social Security funds. The American principle of an exclusively payroll-tax entitlement is something quite artificial which was concocted by the conservative opponents of Social Security in the 1930s and which the Roosevelt administration had to accept in order to get the original Social Security Act of 1935 through the Congress.

What the conservatives feared most then, and what they fear most now, is the prospect of endless demands by workers for increases in benefits. For increases in social benefits are a two-edged sword in the hands of the working class. They not only cut into the current flow of profits but, by increasing the workers’ feelings of security, they strengthen working-class capacity and resolve to fight for higher wages and social benefits in the future. This is a threat to the future flow of profits. To head off such dangerous demands, it seemed essential to the conservatives to be able to confront every worker demand for benefit improvement with the legal requirement of an equivalent payroll-tax increase. And every time such an equivalent has to be computed there are opportunities to skillfully inflate it by pessimistic forecasts of future economic and demographic trends bearing on the cost estimates.

The conservative ploy of the payroll-tax entitlement principle succeeded brilliantly. Most American workers have been taught to be as snobbishly proud of this payroll-tax-based entitlement as they would be of a private home built with their own hands or out of their own savings. Many preen themselves on this form of entitlement and tend to look down with a middle-class sort of contempt on their less fortunate brethren who may have to rely on benefits which are available only after a means-test form of qualification, which is the case with welfare, food-stamps, Medicaid, and rent subsidies.

But if the more than 150 million participants and beneficiaries of the American Social Security System believe that they are entitled to no more Social Security benefits than their payroll-tax contributions justify, they also passionately believe that they are entitled to no less. They have been taught to believe that they have been promised only what they are entitled to and that they are entitled to everything that they have been promised. Many an old-timer still remembers the words of President Franklin D. Roosevelt who said: “We put those payroll contributions there so as to give the contributors a legal, moral, and political right to collect their pensions. With those taxes in there, no damn politician can ever scrap my Social Security program.” The reader will note how the old political fox Roosevelt turned the restrictive principle of payroll-tax entitlement around and made it into a protective principle. He succeeded so well that now the reactionary politicians are indeed “hoist by their own petard.”

In the light of this historical background, no less than the pressure of current needs, it is not surprising that millions of Americans, particularly the senior citizens, have been rudely shocked and badly upset by the evidence emanating from the mouths and actions of the Reagan crowd indicating that they plan to treat the Social Security entitlement programs as just another part of the overall social-welfare budget which they may justifiably slash. Many more of these senior Americans voted for Reagan than for Carter. And of these pro-Reagan voters many supported him because they believed his silly and malicious lies that all that is needed to straighten America out is a vigorous cutback on unjustified social expenditures being madevia welfare, food-stamps, Medicaid, and other means-test programs. Now it is becoming painfully clear that Reagan needs new categories of victims to bleed and that Social Security participants and beneficiaries are scheduled to be included among them.

There are at least two questions that press for an answer. First, how does it come about that Reagan is ready to violate all his election campaign promises and undertake such a politically hazardous and potentially self-destructive project as an attack on the sacrosanct Social Security System? And, second, what sort of a pack of lies is the Reagan crowd concocting in order to convince the potential victims that the planned bloodletting is exclusively intended for their own good and welfare?

With respect to the first question, a glance at any federal government budget projection (it doesn’t matter whether it’s David Stockman’s or the Congressional Budget Office’s) will show that, barring a reversal of Reagan’s tax cuts for the wealthy and the corporations, it’s either the Social Security or the Pentagon share of the budget that’s got to get the axe. And since for the Reagan crowd tax benefits for the wealthy and massive military superiority over the Soviet Union are the alpha and omega of economics and politics, they can see no way out except slashing Social Security and other entitlement programs (such as federal employees’ pensions).

To get down a bit to specifics: in the fiscal 1983 budget there is a prospective deficit, even after the passage of the August 1982 tax-increase legislation, of $150 billion. Now, major expenditure programs for the elderly (Social Security, Medicare, and Federal Employee Pensions) total about $250 billion, while military expenditures and interest on the national debt together require about $320 billion. The rest of the expenditure budget for everything else combined totals up to less than $200 billion. Of this residual $200 billion, social-welfare programs subject to means tests absorb about $70 billion. This means that if every nickel of expenditure for welfare, food stamps, Medicaid, and housing subsidies were to be eliminated there would still be a deficit of some $80 billion, i.e., $150 billion deficit minus $70 billion savings if all means-test programs were eliminated. But since the means-test program had already been cut to the bone by Reagan in 1981 and 1982 and since interest on the national debt is climbing rapidly (because of Reagan tax-cut deficits and high interest rates) there is no way in the world to get the prospective budget deficit down below, say, $100 billion a year other than by cuts in either the military or the Social Security programs.

The Reagan crowd have of course decided that it will be Social Security that has got to be slashed. But to put it over without incurring a political disaster they have to sell the American people on two very big lies. The first big lie is the lie of a current Soviet military superiority designed by the wicked reds for the purpose of conquest of the capitalist world, i.e., the familiar “Russians Are Coming” baloney. The second big lie is that of the impending bankruptcy or insolvency of the Social Security System. The purpose of the first big lie is to get public support for Reagan’s crazy, overblown, military budget. The purpose of the second big lie is to set the stage for the bleeding of the Social Security System so as to provide blood transfusions for the military budget. The rest of this article will be devoted to an exposure of the second big lie.

Insolvency Flim-Flam

If the second big lie can be put over, it will scare the beneficiaries of the Social Security System into accepting without political protest the necessity of cuts in monthly cash benefits in order to prevent a total collapse of the entire system and a total cutoff of all benefits. The pitch the liars make is: You must accept a minor 10 percent or 15 percent cut in cash benefits now in order to prevent a drastic 100 percent cut in benefits later. The effectiveness of the lie depends heavily on the illegitimate application of the notion of the bankruptcy of an ordinary commercial firm to the financial operations of a branch of our national government, which the Social Security System is.

In an ordinary commercial bankruptcy there are two phases. In the first phase a firm gets into difficulty because gross income from sales begins to drop below the cost of labor, materials, and sales and financing operations, i.e., profits become negative. In this first phase the firm goes deeper into debt; it borrows more from banks; it starts slowing up on payments to its suppliers and on the delivery of withheld income and payroll taxes to the government; it also starts pressing its customers to speed up their payments to it. In the second phase the roof caves in and a sudden very big quantitative change for the worse occurs in the unfortunate firm’s cash flow. The banks refuse new credits and demand repayment of old debt; suppliers refuse to ship materials except for cash; the government and other creditors suddenly press their claims vigorously; customers return shipments and slow down on payment of older bills. All of a sudden there is almost no incoming cash flow at all and the firm has to suspend all payments and declare itself bankrupt.

It is because this second phase of total collapse of cash flow can’t possibly occur with a government operation like Social Security that the bankruptcy or insolvency scare about Social Security is so totally phony. About the worst that could happen with Social Security is that the payroll-tax inflow will fall 10 percent or 15 percent short of the cash benefit outflow for a few years.

As we explained earlier the Social Security System operates on a pay-as-you-go, cash-in/cash-out, basis. Payroll taxes are set at levels which, over the long term, are supposed to be adequate to cover cash-benefit payments. Any deficiency in payroll tax rates can be remedied by an increase in the tax rate (usually a very small increase like ¼: percent or ½ percent of wages) or by an increase in the maximum wage base ($32,400 in 1982) to which payroll taxes are applicable. Year-by-year equality between tax inflow and benefit outflow is not possible: as explained earlier, any year-by-year excess of payroll taxes over benefits goes to build up the asset balances in the Social Security trust funds while any deficiency draws down the trust funds. When a trust fund’s assets are decreasing we know that annual cash-benefit outflow is exceeding annual payroll-tax inflow and vice versa.

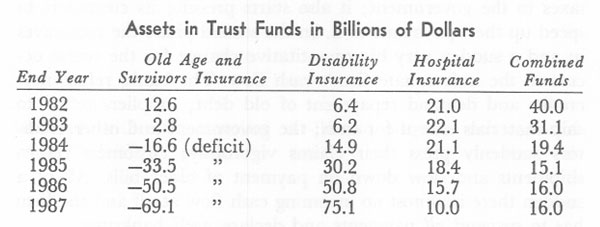

Payroll-tax inflows are, as noted earlier, allocated to three trust funds (see table). According to the projections of the Congressional Budget Office, as reported in the New York Times of June 6, 1982, the prospective asset balances have been estimated as shown in the table. Each asset balance, as we have indicated, represents the accumulation of the annual differences between tax inflow and benefit outflow since the system began to operate, with accrual of interest on invested balances.

All the hue and cry about insolvency stems exclusively from the estimated negative figures for the years 1984 to 1987 in the first column of the above table. It has no other basis whatsoever. Let’s examine and interpret a few of those figures. The Old Age and Survivors Insurance Trust fund shows a positive balance of $2.8 billion at the end of 1983: it’s in the black to that extent, it has that much money in the till. But at the end of 1984 there is the negative balance of $16.6 billion shown, indicating that the fund will then be in the red to that extent. What this means is that during 1984 it is estimated that benefit payments in the Old Age and Survivors category will exceed payroll-tax inflow by $19.4 billion. The latter figure equals the difference between 1984 cash-benefit outflow of $168.4 billion and payroll-tax inflow of $149 billion (none of the last three mentioned figures is shown in the above table). When we subtract the $19.4 billion excess outflow for 1984 from the $2.8 billion asset balance at the end of 1983 we get the $16.6 billion yearend deficit shown in the table for 1984.

How can this deficit be covered so that no Old Age or Survivor beneficiary will have his or her benefits cut down during 1984? The obvious suppliers of funds to cover this deficit are the other two trust funds. For in the aggregate, as can be seen from the fourth column, there is no deficiency at all when the trust funds are combined. The combined asset balance for the three funds never falls below $15 billion. The funds as a whole will never run out of the cash needed to pay benefits according to the Congressional Budget Office projection.

One obvious way to straighten out what is really a very minor difficulty, in spite of the big numbers involved, is to change the allocation of payroll-tax inflow among the three trust funds. As noted, the adequacy of the payroll taxes as a whole to cover benefit outflow is demonstrated by the fact that the combined asset balance in the fourth column of the above table is positive, in the black, for all years. So all you have to do to eliminate the great phony Social Security insolvency crisis is assign more of the payroll-tax inflow to the Old Age and Survivors Insurance Trust fund and less to the Disability Insurance and Hospital Insurance Trust funds.

The so-called insolvency crisis we have been discussing above is often referred to as the Social Security crisis of the 1980s. For the long-range projections made by the Social Security administration show that all the problems of the 1980s will disappear in the 1990s. The reason for that is that the birth-rate was very low during the Great Depression of the 1930s so that the number of workers retiring in the 1990s and in the early years of the next century will be low compared to the number of employed workers paying payroll taxes during those years. According to Robert Myers, former Social Security actuary and Reagan’s choice for Deputy Social Security Commissioner: “The 1990s will be a beautiful period as far as financing the system goes.” Well, if that is so, it suggests another method for remedying any deficiency in the payroll-tax inflow of the 1980s. The Social Security Administration could sell bonds, guaranteed by the federal government and maturing in the 1990s. The bonds would be secured by the excess payroll-tax revenues of the 1990s, and the proceeds of the bond sales would be used to fatten up the Social Security trust funds in the 1980s. Alternatively, the U.S. government could make a temporary unsecured loan to the Social Security System as it did to New York City, Lockheed, and Chrysler.

We have by now suggested three methods of eliminating the great (phony) insolvency crisis of the 1980s without even raising the obvious possibility of a direct grant from the general revenues of the federal government. These methods are: (1) a small increase in payroll-tax rates or an increase in the maximum taxable wage base, (2) a re-allocation of payroll-tax revenue among the three trust funds so as to eliminate the deficit in the Old Age and Survivors Insurance Trust fund, and (3) a borrowing of the excess payroll-tax revenues of the 1990s for use in the 1980s. There are a great many other things that could be done to ease the financing problems of Social Security. One is a reform in the financing and administration of the Medicare and Medicaid Health Care systems. These systems are virtually licenses to steal for the greedy and socially irresponsible doctors, hospitals, and nursing homes of the United States.

Disaster in the Twenty-first Century

There is another type of misrepresentation of the Social Security System which is employed by its enemies and those of social-welfare programs in general. The object here is to convince young people that in the long run, say fifty years down the road, the whole Social Security System is bound to collapse. Even if insolvency is avoided in the 1980s, so that the present generation of senior citizens continue to get their benefits, the prediction is that many of their children, and certainly most of their grandchildren, are going to be cheated out of their benefits when retirement age rolls around for these younger people. The purpose of these scare tactics is to weaken the credibility of the system and soften up its defenders so that opposition to current benefit cuts will be undermined, and to set the stage for abolishing the Social Security System altogether.

As we have already suggested, the finances of the Social Security System will be in good shape from around 1990 to around 2010 because the birth rate was low between 1925 and 1945. For every retired worker on the Social Security benefit rolls between 1990 and 2010 there will be three or more workers contributing payroll taxes and the ratio of the inflow to benefit outflow will produce excesses of taxes over benefits which will fatten up the Social Security trust funds. But after the year 2010 the people born in the great baby boom of the post-Second World War period, starting in 1945, will be reaching age 65, and they will be retiring and receiving Social Security benefits.

About the best analysis we have seen of the emerging problem just referred to is contained in Frank Ackerman’s book Reaganomics (Boston: South End Press, 1982), and we can hardly do better than quote extensively from his analysis. Starting around the year 2010

the ratio of people receiving benefits to people paying taxes into the trust funds will start to soar (unless there is another baby boom in the next decade, producing a surge of new workers by around 2010). By 2030 or so, almost all projections show Social Security, under its present system of financing, in serious trouble. Beyond that, presumably, either astronomical tax rates or lower benefits will be forced on us, if no major changes have been made in the system.

Are lower benefits inevitable? How much security can we afford for the senior citizens of the year 2030? Whatever financing system is used, it is clear that retired people are ultimately fed and clothed by the labor of those who are currently working. But retired people are not the only ones in that position. Children are dependent on current workers in exactly the same way.

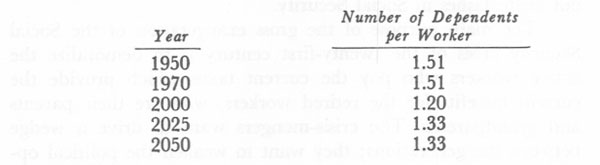

Ackerman then cites studies of the cost of maintaining young and old dependents and concludes that it is reasonable to consider dependents of all ages as placing roughly equal burdens on the working population. This leads immediately to the fundamental question: How many dependents per worker can we afford? Will the burden of dependents on the working population really be so excessive in the year 2030?

Ackerman then shows that standard Census Bureau projections of population combined with other very reasonable assumptions, indicate that there will be fewer dependents per worker in the next century than there were between 1950 and 1970. Here are some figures from Ackerman’s table.

Projecting the population decades into the future is an iffy business, of course. Nonetheless, the Census Bureau’s best available guesses imply that the anticipated crisis in Social Security 30-50 years from now does not reflect any overall increase in the burden of dependents on the working population. If we could afford to live through the childhood of the baby boom generation, we can afford to live through its retirement.

It is clear from this analysis that the problem which will have to be faced in the twenty-first century is the problem of a change in the mix of the dependent population. There will be fewer children and more oldsters. But the overall burden on the working population will not be increased, it will be decreased. Of course ways and means will have to be worked out to smoothly transfer resources which once went to the support of children into the support of the Social Security System. This will undoubtedly involve some application of general government revenue for the support of Social Security, just as in other countries.

Summing Up

The main purpose of the Reagan Social Security crisis-mongers (and their all too many Democratic Party helpers) in grossly exaggerating the “crisis” of the 1980s is to demoralize our retired workers and soften them up, politically, for an immediate cut in cash benefits. The obvious reason that the Reagan crowd can get so much Democratic Party help here is that many of the Democratic politicians are as bad as the Reagan hard-liners when it comes to whipping up hysterical overestimates of Soviet military strength in order to support an insane program of U.S. military and armament expansion, especially in the nuclear field. The Democratic Party hard-liners, too, see no way of feeding the Pentagon the megamillions it demands without deep slashes in Social Security.

The main purpose of the gross exaggeration of the Social Security crisis of the twenty-first century is to demoralize the active workers who pay the current taxes which provide the current benefits for the retired workers, who are their parents and grandparents. The crisis-mongers want to drive a wedge between the generations; they want to weaken the political opposition of the younger workers to the current attack on the benefits of their parents and grandparents. But beyond that the enemies of Social Security want to soften up the many millions of younger workers for a dismantling of the whole system and for its partial replacement by individual insurance and private company pensions.

Thus we may conclude that beyond the immediate goal of providing more current cash for the Pentagon there looms a more important long-term goal which is beckoning the enemies of Social Security. To the latter the system is a debilitating force which is aggravating the weakness of profit and capital accumulation in the United States. They are mobilizing for war on the Social Security System and on the working class it was designed to protect. They seem determined to prove to the world that Marx’s General Law of Capitalist Accumulation is alive and well in America and that our capitalist system demands for its survival a new impoverishment of American workers.

Comments are closed.