This collection of essays is in the nature of a running commentary on some of the main aspects of the turbulent course of capitalist development in the last years of the 1970s and the first of the 1980s. The focus is on the United States, still by a wide margin the biggest of the advanced capitalist countries, but the context is the global capitalist order, including its advanced, less-developed, and underdeveloped components. The first essay in the collection is dated November 1977, the last March 1981, and the summarizing “Introduction” was written in late summer 1981.

What has happened in the year that has passed since then? The answer, essentially, is more of the same.

The recession that began in the second quarter of 1981 (the second in two years) dragged on into 1982. Most observers look for some recovery in the second half of the year, but hardly anyone expects it to be vigorous. Meanwhile, all the typical signs of stagnation continue to be in evidence. The official unemployment rate which stood at 7.6 percent in 1981 rose to 9.5 percent by the middle of 1982, and the manufacturing capacity utilization rate fell from 79.9 percent to 69.9 percent in the same period.

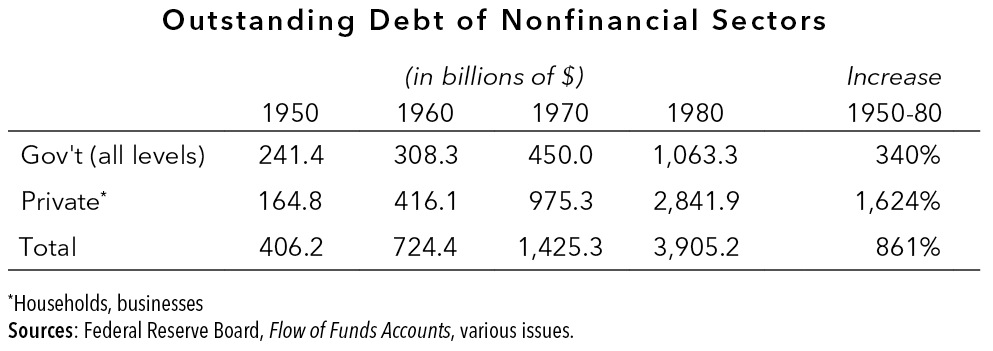

The counterpart to this stagnation in the realm of production and employment was a continuing ballooning of the financial superstructure of the economy which, as the essays in this volume have been at pains to emphasize, has been one of the most spectacular features of capitalist development during the post-Second World War period. The long-term trend is well illustrated by the following figures on the growth of U.S. debt, public and private, from 1950 to 1980.

It will be noted that while government debt, which is emphasized by most observers of the economic scene, grew about four and a half times in the three-decade period, private debt, which is often played down or ignored, was growing more than seventeen fold or nearly four times more rapidly than public debt.

The rate of growth of debt, as usually happens, slowed somewhat in the recessions of 1980 and 1981-82, but this has brought no improvement in the general financial health of the economy. The combination of rising debt, even at a reduced rate, together with faltering profits and continuing high interest rates has wrought havoc with the balance sheets of more and more business firms. Bankruptcies have soared to a postwar high, and liquidity ratios (current liabilities divided by current assets) have continued their long-term decline. Whole sectors of the economy (e.g., construction, much of agriculture, savings banks and savings and loan associations) are on the ropes, and every week brings news of more actual or threatened failures.

Where will it all end? This question is being asked with increasing frequency and urgency. Should we assume that the growing financial weakness of the economy will culminate, as it has so many times in the past, in a panic followed by a debt deflation depression of the kind that overwhelmed world capitalism in the early 1930s? Or have the institutional changes of the post-Second World War period immunized the system against the recurrence of such a catastrophe?

History alone, of course, will provide definitive answers to these questions. But in the meantime it is possible to advance a plausible case for either the optimistic or the pessimistic view. The argument from past experience, never to be lightly dismissed, certainly points to the likelihood, even if not the certainty, of a crash so severe as to defy efforts at control during a painful and possibly protracted deflationary process. We ourselves have always leaned to the view that this is the most probable outcome of the kind of deeply ingrained financial weakening of the economy we are now witnessing.

On the other hand, we are impressed by the counterargument put forward by a number of economists who, though fully aware of the crisis-prone nature of the present financial structure of the United States (and other advanced capitalist countries), nevertheless discount the likelihood of another “Great Depression.” This position has been most persuasively argued by Professor Hyman Minsky of Washington University (St. Louis) whose views are especially worthy of attention precisely because over the years he has been the American economist who has done more than any other to focus on the crucially important destabilizing role of the financial system in advanced capitalist countries.

In his latest pronouncement on the subject (“Can ‘It’ Happen Again?” Challenge [July-August 1982]), Minsky reiterates the opinion he has expressed on various occasions in the past, i.e., that despite a continuing deterioration in the general financial situation, a slide into a depression comparable to that of the 1930s is unlikely. He bases this view on two assumptions: (1) that the Federal Reserve (together with other government agencies such as the deposit insurance corporations) is prepared to play the role of lender-of-last-resort on a scale sufficient to block a chain reaction of the kind that characterized the drastic debt deflation of the 1929-33 period; and (2) that the federal government will continue to run large deficits, thus providing a crucially important cushion of liquidity to the private economy. Both of these assumptions are grounded in the experience of the last two decades: the so-called credit crunches of the 1960s and 1970s have shown how ready and able the federal authorities are to intervene whenever a chain reaction threatens to materialize; and there has been only one year of a balanced budget since 1960, while the outlook for the remainder of the 1980s as seen by the supposedly economy-minded Reagan administration is for vastly expanded deficits.

Minsky’s argument that “It” (i.e., a deep depression) is not likely to happen again is thus a powerful one. There is, however, one factor which is omitted and which, if taken into account, might put a different face on matters. Minsky focuses almost exclusively on the domestic U.S. economy, treating it in abstraction from the vast and vastly complicated international economy of which in fact it forms a tightly integrated part.

In 1974 a relatively small West German bank, Herstatt, which was heavily involved in foreign exchange speculation, collapsed, sending shock waves through the enormous and basically unregulated Euromoney market. The danger of a chain-reaction catastrophe was averted when the central banks proclaimed what came to be known as the Basle Concordat according to which the supervisory responsibilities of each central bank were specified in the event of a potential destabilization of the international money market. The wording of the agreement, however, was imprecise and the agreement itself was merely a statement of intent with no legal force. Among other things, nothing was said about the responsibility of bank holding companies such as the Banco Ambrosiano Holdings (BAH), whose failure is currently disturbing the 200 banks that had lent money to it. The nature of the potential risks in the international banking community was clarified in a recent column in the New York Times (July 2, 1982) by Karen Lissakers, a Senior Associate of the Carnegie Endowment for International Peace. Using the massive Western loans to the countries of East Europe for illustrative purposes, Lissakers wrote:

While the direct East European loan exposure of United States banks is a modest $7 billion, their indirect exposure through the interbank market is enormous. American banks have not only made loans to Poland and the rest, they have also made loans to other Western banks that have in turn lent to Eastern Europe.

European banks have some $40 billion out to the East bloc. European banking authorities have assured the United States that none of their banks would be rendered insolvent by having to write off the Polish loans. But a simultaneous default or even extended payment arrearages by Poland, Rumania, and Hungary, for example, would be a different story….

If some European banks experience liquidity problems because the Communist countries are not paying on time, United States banks could become involved via the intricate web of interbank loans, revolving credits, and overnight placements that link the global capital market.

It should perhaps be interposed here that what is said about loans to Eastern Europe would apply, mutatis mutandis, to loans to Third World countries which in aggregate are vastly larger. Lissakers continues:

This interbank market increases the efficiency of the world economy by allowing the excess savings in one part of the globe to move swiftly to borrowers in another. And the intermediation of a chain of banks between the depositors’ and ultimate borrowers spreads the risk of international lending. “Wholesale” lending by banks to other banks, in fact, accounts for 70 percent of the Eurocurrency market.

But many banking experts have come to regard the interbank market as the Achilles heel of the international financial system. For if the interbank market can swiftly transmit funds from one part of the system to another, it can just as rapidly transmit—and spread through the system—the problems of any one bank.

The market can lose confidence in a bank that is known to have large loan losses. The bank may then find that deposits that were routinely renewed at maturity are now withdrawn, and other banks close off needed lines of credit. Suddenly the bank cannot meet its obligations to other depositors and banks from which it has borrowed; banks that were counting on these payments in turn find themselves scrambling for funds to cover the unexpected shortfall and so on along the chain.

The result is a sudden contraction of the market. Herstatt’s collapse instantly caused the Eurocurrency market to shrink by 50 percent.

Swift intervention by a central bank to cover the obligations of an insolvent commercial bank can isolate the problem and keep a single failure from rippling through the system. But no central bank may answer the bell in the absence of prior agreement on who is responsible.

Citibank’s Walter Wriston said in 1979, “Whether we like it or not, mankind now has a completely integrated, international financial and informational marketplace capable of moving money and ideas to any place on this planet in minutes.” The machine is also capable of stopping. Mr. Wriston and his colleagues—whether they like it or not—need the kind of government regulation and support that prevent abuse of the system when everybody is happy and keep the wheels turning when everyone is sad.

A relatively simple thing, one might think. And yet far from securely attained—and perhaps unattainable.

New York

August 15, 1982

Comments are closed.