In the last few years the idea of a “New Economy” has gained wide currency, almost rivaling “globalization” as a neologism that characterizes our era. Thus The Economic Report of the President, 2001, begins: “Over the last 8 years the American economy has transformed itself so radically that many believe we have witnessed the creation of a New Economy.” This New Economy is seen, first and foremost, as consisting of those firms and economic sectors most closely associated with the revolution in digital technology and the growth of the Internet. The rapid convergence of information technologies—including computers, software, satellites, fiber optics, and the Internet—has, it is believed, fundamentally altered the economic landscape. Since the mid-1990s, these revolutionary technological developments have, it is argued, spilled over into the wider economy, generating higher productivity growth, a sustained acceleration of economic growth, lower unemployment, lower inflation, and an attenuation of the business cycle.

For many the focal point of the New Economy has been the highflying technology stocks that carried stock market speculation to new giddy heights during what has come to be known as the “millennium boom.” This was rationalized by business (though with growing nervousness after the sharp fall in technology stocks in the second half of 2000) as a measured response to the opportunities offered by the New Economy—and not simply a speculative bubble. Meanwhile, a vast new wave of corporate mergers beyond anything ever seen before has been taking place—for which the dual rationale is globalization and the rise of the New Economy.

No one has been a stronger proponent of the New Economy thesis than Federal Reserve Chairman Alan Greenspan. In a speech on “Structural Change in the New Economy” delivered to the National Governors’ Association on July 11, 2000, Greenspan argued that “it is the proliferation of information technology throughout the economy that makes the current period appear so different from preceding decades…One result of the more-rapid pace of IT innovation has been a visible acceleration of the process that noted economist Joseph Schumpeter many years ago termed ‘creative destruction’—the continuous shift in which emerging technologies push out the old.” Among the advantages of the New Economy is the ability of corporations to generate a flood of information in miniseconds, allowing them to “reduce unnecessary inventory and dispense with labor and capital redundancies.” In a speech on “The Revolution in Information Technology” delivered at Boston College on March 6, 2000, Greenspan claimed that “until the mid-1990s, the billions of dollars that businesses had poured into information technology seemed to leave little imprint on the overall economy.” But beginning in 1995 that changed, and the spillover effects of digital technology are revolutionizing Old Economy sectors, making the New Economy a more universal phenomenon. “Computer modeling, for example, has dramatically reduced the time and cost required to design items ranging from motor vehicles to commercial airliners to skyscrapers.”*

The New Economy has also been associated with the development of a more flexible workforce: non-unionized, highly mobile, just-in-time workers, sometimes embodying new job skills. Comparing the more highly unionized labor forces of Europe and Japan to that of the United States, Greenspan stated in July 2000 that “the relatively inflexible and, hence, more costly labor markets of these economies appear to be a significant part of the explanation [as to why the New Economy has been slower to develop there]. The elevated rates of return offered by the newer technologies in the United States are largely the result of a reduction in labor costs per unit of output. The rates of return on investment in the same new technologies are correspondingly less in Europe and Japan because businesses there face higher costs of displacing workers than we do.”

The existence of the New Economy, in the sense of the advent of a dynamic information technology sector within the economy that has been a spur to accumulation, is not to be doubted. Clearly, it constitutes something distinct in the history of capitalism. Two other ideas associated with the New Economy are, however, more open to question. First, it is contended that the New Economy constitutes a new technological-industrial revolution, comparable to the introduction of the steam engine or the automobile in its effect on the overall economy, and that it is remaking the entire Old Economy in its image, ushering in a new era of permanently higher productivity. According to Fortune magazine (June 8, 1998), “The [computer] chip has already transformed our lives at least as pervasively as the internal-combustion engine or the electric motor.” Second, it is often suggested that the New Economy has attenuated, if not altogether eliminated, the business cycle. Thus Thomas Petzinger Jr. observed in the Wall Street Journal (December 31, 1999) that “the business cycle—a creation of the Industrial Age—may well become an anachronism.” In the balance of this piece, we will take a look at these two claims.

A New Industrial Revolution?

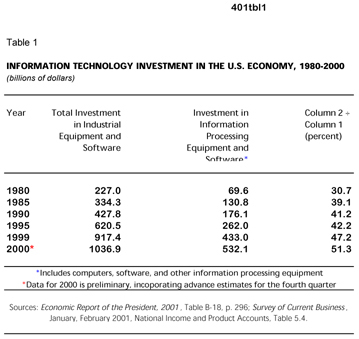

Some idea of the importance of the New Economy sector to the overall economy can be seen in the fact that although information technology only accounted for at most about 6 percent of GDP during the third quarter of 2000, about a quarter of the total economic growth since 1995 can be attributed to this sector together with telecommunications.* As shown in Table 1, the share of information technology investment in total investment in industrial equipment and software (equal to total private non-residential fixed investment minus investment in structures) rose from less than one-third in 1980 to more than one-half in 2000.

Are we then witnessing a new industrial revolution, equivalent to the first industrial revolution, which began at the end of the eighteenth century (centered on the steam engine), or the second industrial revolution, which began at the beginning of the twentieth century (centered on the automobile and electricity)? For many purveyors of the New Economy idea, not only is this a new industrial revolution, but it is this which has suspended all economic laws, including the business cycle, pointing to a period of long-term, rapid growth, with no foreseeable end.

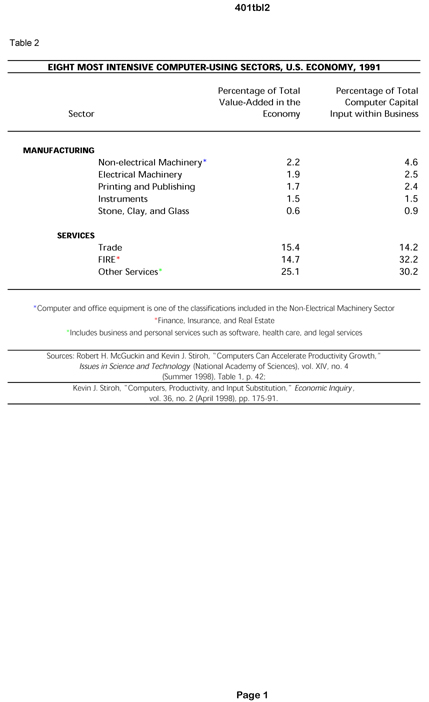

The facts, however, support none of this hype. In this connection it is useful to distinguish between the sector that produces computers and where these products are used in the business economy. Contrary to a widespread view, computers are not used equally everywhere within business. Conference board economists Robert H. McGuckin and Kevin Stiroh have provided an analysis of the eight private sectors of the economy that use computers most intensively—each with more than 4 percent of their capital in the form of computers. This includes three service sectors—trade, FIRE (finance, insurance, and real estate), and other services, and five manufacturing sectors—non-electrical machinery, electrical machinery, printing and publishing, instruments, and stone, clay, and glass. The percentage of total value added in the economy and the share of computer capital input within business accounted for by each of these industries in 1991 are shown in Table 2. Most significant is the fact that 76.6 percent of all computer input within business in 1991 occurred in trade, FIRE, and other services (which encompasses various personal services, including legal services, healthcare and software). Only 11.9 percent of computer input into business is accounted for by the five computer-intensive sectors in manufacturing listed in Table 2, and a further 11.5 percent by twenty-seven other industries (including agriculture, mining, transportation, construction, communication, and public utilities, among others).

To be sure, the structure of demand for computers shown here is partly a reflection of the enormous weight in the economy assumed by services, and particularly financial services. But a technological revolution that finds more than three-quarters of its business demand in the service industries (including finance, retail and wholesale trade, marketing, legal services, health services, entertainment, and other personal services) may be seen as falling somewhat short of an all-round “industrial revolution.”* The service industries, rather than representing high productivity growth in the economy, generally represent just the opposite (if productivity growth means anything in this context).*

Indeed, when it comes to an empirical examination of the New Economy thesis that the digital revolution since the mid-1990s has heightened productivity throughout the economy, the most that can be said is that there still is little or no hard evidence that computers have generated much progress in this area. The upturn in productivity, which accompanied the upturn in the business cycle, has naturally encouraged the view that this can be explained by the information technology revolution. But is the jump of 1.33 percentage points in average annual rate of productivity growth—which rose from 1.42 percent in 1972-1995 to 2.75 percent between fourth quarter 1995 and fourth quarter 1999—really a result of the productivity-enhancing effect of information technology, spilling over into the overall economy? This question has been taken up most systematically by Robert J. Gordon, professor of economics at Northwestern University. Gordon “peels the onion” of productivity growth to show a surprising explanation, very different from the received truth in the establishment and the public. Gordon looked into the various factors contributing to the leap in rates of productivity. He explains and demonstrates the effect of a variety of contributing factors such as the cyclical upturn of the economy, technological acceleration in the production of computer hardware, and technological changes in factories producing durable goods. His striking result is that the contribution computer use has made is surprisingly low. Of the 1.33 percentage-point rise in productivity growth referred to above, only 0.07, “a mere pittance,” can be attributed to the use of computer technology and software outside of durable goods production. In sum, he found that the effect of digital technology on productivity was small on the whole; such advance as there was took place almost entirely in the manufacture of durable goods.*

It is of course widely believed that the rapid expansion of the Internet has been the device that has allowed the productivity effects of the New Economy to diffuse throughout the economy. But the facts, as Gordon’s analysis of productivity has shown, do not warrant such a conclusion at present. Computers are widely available in offices, but rather than increasing the productivity of business, the opposite effect often seems to apply, as employees use their corporate Internet access to look up stock quotes related to their personal investments, to do online shopping, or to carry on e-mail correspondence. Studies show that consumer oriented web sites get their highest usage not in the evenings or on weekends, but in the daytime, Monday to Friday, when people are at work. The proliferation of laptop computers, faxes, satellites, the Internet, etc., has dramatically altered the newspaper business, yet between 1987 and 1997 productivity in the newspaper industry dropped by an average annual rate of 2.3 percent (John Cassidy, “The Productivity Mirage,” The New Yorker, November 27, 2000, p. 116).

The digital revolution certainly is a technological revolution with widespread effects; the important thing from an economic standpoint, however, is that it is not epoch-making, as in the case of the steam engine, the railroad, and the automobile. It still has not produced “a radical alteration in economic geography with attendant internal migrations and the building of whole communities,” each requiring or making possible the production of numerous new goods and services, on the same scale as did the steam engine, the railroad, or the automobile in the first and second industrial revolutions (Paul Baran and Paul Sweezy, Monopoly Capital, pp. 219-20).

The Taming of the Business Cycle?

The economic expansion that began in March 1991 has been accompanied by an explosion of stock market valuations and of corporate (and consumer) debt. As Yale economics professor Robert Schiller observed in his book Irrational Exuberance,

The Dow Jones Industrial Average…stood at around 3,600 in early 1994. By 1999, it had passed 11,000, more than tripling in five years…. However, over the same period, basic economic indicators did not come close to tripling. U.S. personal income and gross domestic product rose less than 30%, and almost half of this increase was due to inflation. Corporate profits rose less than 60%, and that from a temporary recession-depressed base. (page 4)

The “millennium boom,” Schiller goes on to observe, is the “largest stock market boom ever.” Price-earning ratios (the real S&P Composite Index for stock prices divided by the ten-year moving average of real corporate earnings on the index) hit 44.3 in January 2000, the highest level ever recorded up to that time, with the closest historical parallel in September 1929 (just before the stock market crash), when the ratio hit 32.6. For Schiller and many others the dizzying inflation of share prices on the stock market has all the characteristics of a classic speculative bubble, traceable to factors that have nothing to do with “rational economic fundamentals,” given the much slower relative growth of earnings.

Significantly, it was Alan Greenspan, in a speech in Washington on December 5, 1996, who coined the term “irrational exuberance” to describe this dangerous situation. Here it is worth noting that there are a number of problems facing Greenspan in his role as Federal Reserve Chairman. He must try to keep the economy flying high as long as possible, and help to engineer a soft landing when it is not. Both of these aspirations are of course well beyond the powers of any individual or any institution, including the Federal Reserve Chairman and the Federal Reserve Board. Hence, a certain amount of “jawboning” designed to influence the markets is part of the game. Greenspan’s statements have often been aimed at calming down the speculating, lest the market take a major dive and upset the apple cart, while also serving to warn business that there is a very real danger. At the same time his pronouncements more generally are aimed at rationalizing for investors the anarchy of the market, in order to build a general sense of stability and confidence. Thus just months after his “irrational exuberance speech,” Greenspan was extolling the virtues of the New Economy. The ballooning of stock valuations and the seemingly overrapid growth of the economy in general were not irrational in the main, but were in large part justified by the productivity expansion brought on by the New Economy. It was now possible to have lower unemployment without the threat of inflation—precisely because of this growth of productivity. As it is now commonly put in the economic literature, the “speed limits” of the economy had changed.

Over the course of every long boom in the history of industrial capitalism, economic interests have sought to account for continuing growth and stock market expansion by arguing that a New Era has arisen, which has tamed, or even eliminated the business cycle. Such New Era pronouncements are always rooted in some notion of changing technology and/or business organization. Prior to the 1929 stock market crash that introduced the Great Depression, it was commonly argued that a New Era had emerged with the growth of the large monopolistic capitals, which were able to manage and regulate the economy more efficiently, smoothing out the economic swings and decreasing or eliminating the downswings altogether. Irving Fischer, professor of economics at Yale, and the most prestigious U.S. economist of his day, is reported to have declared, on the basis of such New Era thinking—just prior to the stock market peak in 1929 (which was closely followed by the crash)—that “stock prices have reached what looks like a permanently high plateau” (quoted in Schiller, Irrational Exuberance, p. 106).

Similar views are being promoted today. For example in a July/August 1997 article entitled “The End of the Business Cycle?” for Foreign Affairs (the leading U.S. foreign policy journal, published by the Council for Foreign Relations), Steven Weber argued that “Changes in technology, ideology, employment, and finance, along with the globalization of production and consumption, have reduced the volatility of economic activity in the industrialized world. For both empirical and theoretical reasons, in advanced industrial economies the waves of the business cycle may be becoming more like ripples.”

Greenspan himself, though hardly claiming that the business cycle has been eliminated, has suggested, as we have seen, that the increased control of inventories resulting from the development of computerized information systems and just-in-time production has enormously reduced the forces generating recession. “Prior to the IT revolution,” he argued in a speech before the Joint Economic Committee of Congress on June 14, 1999, “the paucity of timely knowledge of customers’ needs and of the location of inventories and materials flows throughout complex production systems” necessitated the maintenance of “substantial programmed redundancies,” including “doubling up on materials” if businesses were to function properly. In the New Economy, however, business management has been able “to remove large swaths of inventory safety stocks and worker redundancies.” The advent of processes such as bar-scanning devices and satellite location of trucks has reduced delivery times. The growth of Internet Web sites has speeded up and in some cases streamlined the way business transactions are conducted.

Moreover, along with his claim that structural productivity growth has shifted upward with the advent of the New Economy, Greenspan also insists that wages have been kept down and unit labor costs restrained by increased job insecurity of workers at any given level of unemployment, due to globalization and the creation of more flexible labor markets, which are taken as hallmarks of the New Economy. Consequently, workers threatened by “flexibility” (which has often meant the growth of non-standard and contingent jobs, such as work through temporary help agencies) opt for job security where possible rather than rocking the boat with wage demands. In testimony before the Joint Economic Committee on March 20, 1997, Greenspan noted: “In 1991, at the bottom of the recession, a survey of workers at large firms by International Survey Research Corporation indicated that 25 percent feared being laid off. In 1996, despite the sharply lower unemployment rate and the tighter labor market, the same survey organization found that 46 percent were fearful of a job layoff.”

The argument on job insecurity, which focuses on a more intense class struggle imposed from above and the increasing costs of losing a job (particularly given the rising indebtedness of the working class), gets closer to the truth in explaining why “wage inflation” did not ignite during the economic expansion, than do claims regarding structural improvements in productivity. Nevertheless this argument, like all other dominant economic perspectives, suffers from a view of the business cycle ushered in by monetarism and Reaganomics that sees inflation (especially so-called “wage inflation”) as the primary cause of recessions. The truth is that economic downturns have more fundamental causes related to accumulation, the buildup of overcapacity, etc., that are relatively independent of mere price movements. It is not a squeeze on profit margins, due to rising wage costs—supposedly forcing firms to raise prices—that generally accounts for the onset of economic crisis. More important is the overinvestment and overexpansion of debt that occurs whenever the forces that initially propelled the boom start to peter out. And underlying this of course are structural problems of overexploitation, uneven distribution of income of wealth, and lack of effective demand that are always present under capitalist conditions. Such basic truths of accumulation, which were widely acknowledged in the days of the Keynesian revolution, remain as valid today as ever—the New Economy notwithstanding.

The deceleration of real GDP growth in the fourth quarter of 2000, dropping from 2.2 percent in the third quarter to 1.1 percent in the fourth quarter, generated widespread concern within business. Most ominous was the fact that real nonresidential fixed investment fell 0.6 percent in the fourth quarter, as opposed to a rise of 7.7 percent in the third, with investment in equipment and software declining by 3.5 percent. All of this occurred simultaneously with a dramatic drop in the NASDAQ stock index (dominated by dot-coms), followed by a general decline on the New York Stock Exchange.

Whether these events presage a full-fledged economic crisis, no one knows at this point (late February 2001). What is significant, however, is the surprise with which this apparent turnaround was viewed even in supposedly knowledgeable quarters. Some had clearly come to believe, history notwithstanding, that periods of rapid technological progress were themselves guarantees against business downturns. Others had bought into the idea that the New Economy was new precisely in the New Era extra-economic sense of overcoming the business cycle. The point to remember, however, is that business cycles have been a regular feature of capitalism since the early part of the nineteenth century and continue to live on despite dreams about the flood of information available to corporations in miniseconds, and similar notions. None of the empirical and theoretical claims associated with the New Economy—technological revolution, rising productivity, rising profit margins, and the like—are proof against the business cycle. Indeed, cyclical downturns most often occur not in spite of but because of such developments. That is, a high rate of accumulation can itself lead to crisis. Overexpansion of capacity relative to consumer buying power is an essential feature of a capitalist economy throughout its history—in the state of competitive capitalism, in the monopoly stage, and in the current phase of accelerating globalization and new technology.

Nor is the expansion of the financial system, including the participation of more and more people in speculative markets, a guard against crisis. Financial crises, like economic crises more generally, are endemic to accumulation under capitalism. Such economic instability arises not from mismanagement, shortage of information, or lack of business and consumer confidence, but from the dynamics of class-based accumulation. The outstanding contribution made by the new technology in creating mountains of information that can spread around the world at the speed of light can contribute to a meltdown of the money markets as effectively as it contributed to its ballooning. News or hints of a break in the fragile financial network, which is based on thinly spread layers of debt, can reach the money market headquarters with a speed too fast for central banks to prevent a chain reaction on the way down.

Next to Greenspan himself, Michael Mandel, economics editor for Business Week, has probably done more than anyone else to propagate the current New Economy hype. Yet, instead of arguing that the New Economy is impervious to the business cycle, Mandel has recently written a book, entitled The Coming Internet Depression, that points to the probability of a severe New Economy crisis, arising specifically out of what he calls the “tech cycle.” The tech cycle, Mandel argues, stands for the fact that “the business cycle has been reincarnated in a different garb for the information age.” The expansion phase of the tech cycle, he says, is characterized by rapid technological innovation; easy available funding for start-ups (as a result of venture capital); strong productivity growth; investment booms as companies scramble to keep up with the technology; the holding down of inflation due to productivity gains and competitive pressures; and buoyant stock markets. All of this conveys the main thrust of the New Economy idea. But Mandel says that there is also a contraction phase to the New Economy’s tech cycle: technological stagnation; the drying up of venture capital; weak productivity growth; falling investment; rebounding inflation; and depleted stock markets. Insofar as the tech cycle is seen as displacing the traditional business cycle, Mandel’s analysis is altogether questionable. But his claim that the various forces that sent the New Economy up can also, once these forces have been spent, lead to its turning down—and indeed account for a drastic downturn—adds an element of rationality to the New Economy hype. High tech, Mandel argues, means “high volatility.”

Making things even more perilous, Mandel argues, is the extent to which the New Economy boom has been financed by debt, both corporate and household, which introduces the possibility of cascading defaults. The ratio of household debt to disposable income rose from 80 percent in 1989 to around 100 percent today.* The debt of nonfinancial corporations, meanwhile, rose by 34 percent between the beginning of 1997 and the beginning of 2000. Such extensive borrowing means more pain in the downturn of the cycle—particularly for workers who have borrowed out of necessity to compensate for stagnant real wages.

It is also worth noting that the United States benefited in the 1990s from the relative prosperity of its economy in relation to Europe and Japan. An economic resurgence in Europe and Asia, however, Mandel warns, could “trigger a financial crisis in the U.S., and perhaps even globally.” The New Economy boom in the U.S. had been financed to a considerable extent by an expanding flow of money from overseas. “In 1995,” he notes, “foreign money was only 8% of total U.S. investment (residential and business). By the first quarter of 2000, foreign money had risen to 26% of total investment.” All of this has made the U.S. a net debtor on a massive scale, “with the value of its overseas liabilities exceeding the estimated value of assets overseas by more than $1 trillion at the end of 1999.” It is conceivable that such conditions could lead to a devastating run on the dollar causing foreign investors to pull out their investments even more quickly than they put them in. This could generate a global financial crisis. With “a sell-off of the dollar,” as economists John Eatwell and Lance Taylor wrote in Global Finance at Risk, “the potential disequilibria—portfolio shifts away from the U.S., bigger international obligations on its debt, and growing financial stress on the household sector—could begin to feed on one another and on the views of the markets. At that point…all hopes for global macro stability could disappear.” The globalization of the disastrous consequences of a New Economy bust could generate a world economic meltdown.

Michael Mandel’s book, following the competitive dictates of the business-press market, is subtitled Why the High-Tech Boom Will Go Bust, Why the Crash Will Be Worse than You Think, and How to Prosper Afterwards. This is prognostication and hyperbole, not science. Although it is entirely rational to recognize that the New Economy thesis, even if assumed correct, has its downside, which could lead to a severe crisis, it is well to remember that much of what is taken as already proven about the New Economy is illusion. The investment boom associated with the digital economy is real. But the thesis that there has been a structural (not cyclical) elevation of productivity throughout the whole economy, and that this (rather than the class struggle and the restructuring of the labor market) accounts for relatively high employment accompanied by relatively low inflation, is extremely doubtful at best. Indeed, the commonsense economic assumption that higher productivity automatically means higher economic growth is itself questionable. Some of the fastest expansion of jobs and value-added in the U.S. economy in recent decades has been in those sectors—services, and especially financial services—that are notorious for their low productivity gains, and that are associated with the accumulation of money capital rather than the expansion of production.

Hence, the economic downturn that now appears to be upon us will most likely have much more in common with a classic business cycle, in which the central role is played by the buildup of overcapacity, than with the “tech cycle” described by Mandel. Indeed, excess capacity is now appearing in industry after industry and on a global scale. As reported by Floyd Norris in the New York Times (February 16, 2001), the global telecommunications industry—the highest of high-flying sectors of the late-90s boom—is facing a “black hole.” The enormous capital expenditures have created capacity that far outruns demand. And credit has dried up, even as vast sums are needed to complete massive projects already well underway. “Weaker companies, meanwhile, are failing. ‘Piece by piece, they are starting to default up the chain,’ said Charles Clough of Clough Capital, a money management firm…. Eventually, there will be growth to absorb the excess capacity. But that will take years, not months. The financial markets have still not fully discounted the pain to come.”

There is no question about the fact that the magical new technology of the information age has dramatically changed aspects of personal and social life. It promises to do even more as time goes by. Indeed, all major technological revolutions over the course of capitalist development have contributed their share in altering the way we live. But in no case did any of these earlier technological revolutions create a new economy, or a new tech cycle, any more than has today’s digital revolution. The economic laws of motion of capitalism remain in force.

We are living through an unprecedented situation marked by dramatic new developments, including not only the New Economy boom and bust, but also an unheard of polarization of wealth, rampant globalization, and the greatest merger wave in history aimed at the takeover of larger and larger sections of the world market by a relatively small number of global-monopolistic corporations. Rather than trying to predict what will happen under these rapidly changing circumstances we should be keeping our eyes on the main contradictions and tendencies that will feature prominently in any future developments, recognizing all along that this is a phenomenon of capital accumulation and crisis—and hence class struggle.

Notes

*For Greenspan’s speeches see the Federal Reserve Board website: http://www.federalreserve.gov

*Estimates on the contribution of the New Economy to economic growth are those of the Bureau of Economic Analysis. See J. Steven Landefeld and Barbara M. Fraumeni, Measuring the New Economy, Bureau of Economic Analysis Advisory Committee Meeting, May 5, 2000, Table 2 http://www.bea.doc.gov/papers.htm. U.S. government statistics use what is called a “hedonic price index” to make adjustments for quality improvements, in accounting for real computer spending. This tends to overstate information technology spending in the U.S. and its contribution to GDP compared to the majority of countries (exceptions being Canada, France, and Japan) that do not use such hedonic indices. See Economic Report of the President, 2001, pp. 164-65.

*It should be noted that there have been major advances in the use of automatic machinery within industrial production as a result of the new technology. This includes not only computers but cybernetics, which has a lot to do with the whole computer technology. To get more automatic, workerless production equipment, various devices of automatic controls and feedback, which use computers or computer-like instruments are introduced. Hence, data on the utilization of pure information technology within durable manufacturing, such as referred to here, may be somewhat misleading, understating the role that the new technology plays in that sector.

*On the problems of the application of productivity statistics to the service sector, see Harry Magdoff and Paul M. Sweezy, “The Uses and Abuses of Measuring Productivity,” Monthly Review, June 1980.

*Robert J. Gordon, “Not Much of a New Economy,” Financial Times, July 26, 2000, and “Does the ‘New Economy’ Measure Up to the Great Inventions of the Past?,” Journal of Economic Perspectives, vol. 14, no. 4 (Fall 2000), pp. 49-74.

*See the Editors, “Working-Class Households and the Burden of Debt,” Monthly Review, vol. 52, no. 1 (May 2000), pp. 1-11.

Comments are closed.