In The Political Economy of Growth and in an article he wrote several years earlier, the economist Paul A. Baran noted how, in an economic system characterized by a hierarchy of classes where economic and political power is concentrated at the top, the output and income beyond what is consumed by most people (food, clothing, housing, public safety, education, and so on) mostly goes to the highest class. This extra portion is what he called the economic surplus, a form of savings or income left over after consumption. In a feudalistic system, there is little incentive to use the proceeds of this type of surplus to buy more tools and equipment for more production of output and income. The lord or baron has little incentive to lend or give serfs money because he may not benefit from any increased productivity. It is with capitalism that such incentives to reinvest in production become important.

Recently published and estimated historical data illustrate Baran’s analyses of feudalism. Such data show that the economic surplus declined during the thirteenth and fourteenth centuries in England, which helps explain the “crisis of feudalism” that started in the thirteenth century. It was not until several centuries later, when capitalism became the dominant economic system, that the economic surplus began to rise on a consistent basis, probably due to the reinvestment of a portion of the surplus into productive activities, a greater ratio of capital income to rental income, and a greater ratio of investment to economic surplus. However, somewhat surprisingly, by the nineteenth century the surplus still did not attain the levels reached in the thirteenth century.

Background

The scholarly literature on the causes of the decline and end of feudalism in Western Europe is vast, and it is impossible here to give credit to all those who have contributed to these studies. Although not a primary participant in the debate among economists known as the Dobb-Sweezy debate, Baran saw the critical flaw in feudalism as one in which the output and income created beyond the amount necessary to meet society’s needs was basically wasted by the aristocracy and church through spending on grand castles, cathedrals, minstrels, and wars of conquest and plunder.1 Baran labeled such extra output and income actual economic surplus, as distinct from potential economic surplus.2 The latter is the actual economic surplus that would be obtained if society’s labor and capital were fully and productively employed (such as in farming and making clothes) and not channeled into unproductive activities, such as those pursued by noblemen and clergy during feudalism or activities such as advertising, defense expenditures, and excessive managerial compensation under capitalism. Baran goes as far as calling noblemen and clergy “parasites” thriving off the output of serfs.

The concept of an aggregate, actual economic surplus, as distinct from the concept of economic surplus in supply-and-demand analysis, was later further developed by Baran and Paul M. Sweezy.3 Sustained economic growth occurs through absorption of the surplus by investment in capital goods (tools, plant and equipment, new businesses, and new technology) or by the government investing more money in education, infrastructure, or health care. This is carried out in most developed, capitalist economies, but was not really done in any form under feudalism. In The Political Economy of Growth, Baran concludes that the economic and political leaders of many developing economies in the world are either large landowners or mine owners, or are simply representatives (“compradors”) who run their nations in a feudalistic manner while allowing their economies to be exploited by the foreign capitalist interests of more developed economies. Such exploitation keeps many of these societies on the periphery of the global economy and keeps them in an underdeveloped economic state.

Within the last twenty years or so, different estimates of English medieval economic activity have been published, comprising perhaps the most detailed measures of economic records when compared to databases on other European nations and regions. Gregory Clark has published data on national income accounts, population, prices, wages, and land rents for England from 1209 to 1868. He has estimated wage, capital, and land rent shares of national income using estimates of pay, work days, interest rates, values of ships, iron works, and estimates of farm, public works (canals, roads, and bridges), and real property values.4 S. Broadberry and colleagues have written a book containing some estimates made by Clark and others, as well as their own numbers on English and British wages, prices, population, gross domestic product (GDP), real GDP, and real GDP per capita, among other economic measurements from 1270 to 1870.5 Using this data, I show how Baran’s concept of the economic surplus and a new concept introduced by Zhun Xu in 2019, the Baran ratio, can be used to partially explain and describe the transition from feudalism to capitalism and any possible transition from capitalism to some other type of economic system.6

Analysis

One can try to estimate Baran’s economic surplus for England by combining Clark’s estimates of English capital income, land rent, farm income, indirect taxation, and housing rent, and dividing this by Clark’s estimate of net national income (NNI). With the exception of some taxation revenues, capital income, land rent income, housing rent income, and some government tax revenues (such as those going to help monarchs and their families personally) would represent amounts accruing mostly to those of the upper classes in a feudalistic society or transition economy, just as profits, interest, dividends, royalties, and rental income accrue to the upper class of a capitalistic society, with tax revenues often benefiting the military (“wasteful expenditures,” according to Baran) or more necessary social programs, especially educational expenditures.7 The exception to capital income accruing to the upper class would be the income earned off capital and garnered by small farmers who did not serve a lord, although as time passed this income grew and became more and more concentrated in the hands of large landowners and a landed gentry. To be more consistent with the concept of economic surplus, one would also have to estimate the value of, or expenditures on, activities that Baran and Sweezy claimed were unproductive or wasteful. In a capitalistic society, such activities include advertising, marketing, distribution, finance, insurance and real estate services, militarism, and research and development on things such as package design or color.8 For a feudalistic society, Baran claims that such unproductive activities would be the building of grand cathedrals and castles, the employment of minstrels and court jesters, and spending on legions or armies designed to control the peasantry or to engage in wars of conquest and plunder. These endeavors provide no “use” value in sustaining or promoting human life and add no future productive activity to an economy.

As Baran notes, Thomas Malthus thought the aristocracy spending so much on frivolous things meant that there would be a stimulus effect on the medieval economy. Adam Smith, however, was critical of the employment of unproductive labor and spending on unproductive pursuits.9 Unfortunately, the estimates do not include enough detail for a long enough period of time to quantify such unproductive activities. Therefore, estimates of capital, land and home rental income earned, and taxes collected are used to estimate economic surplus.

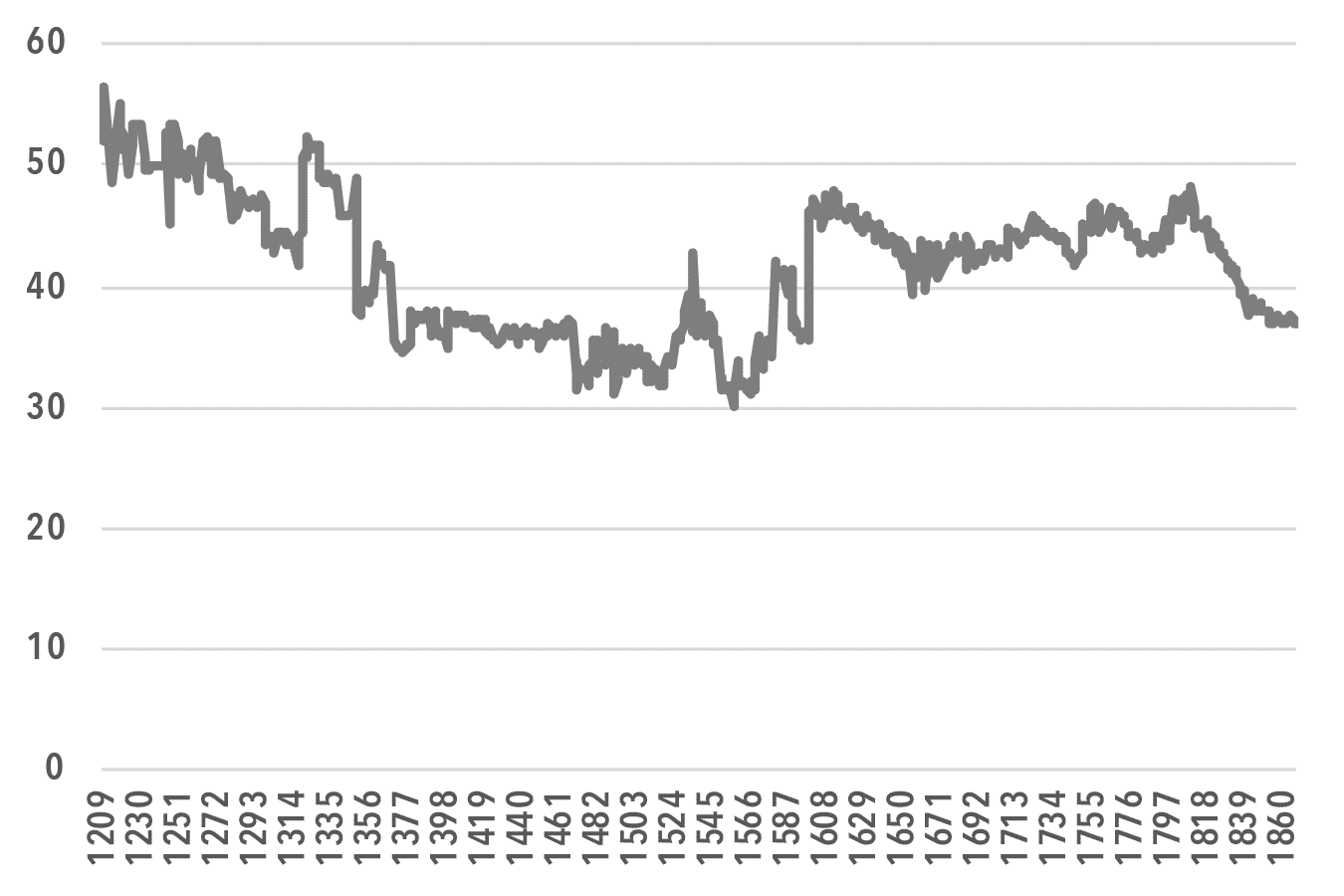

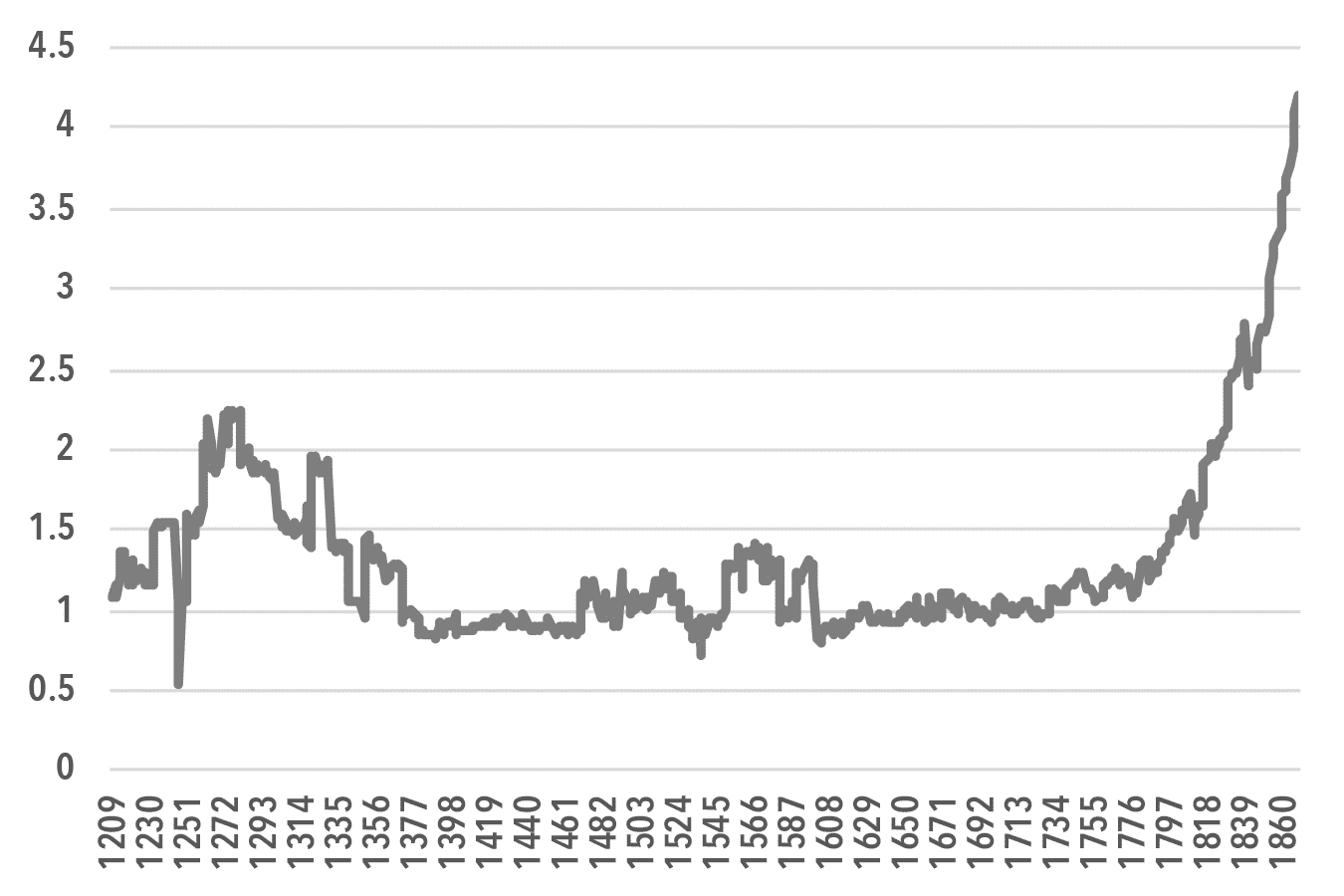

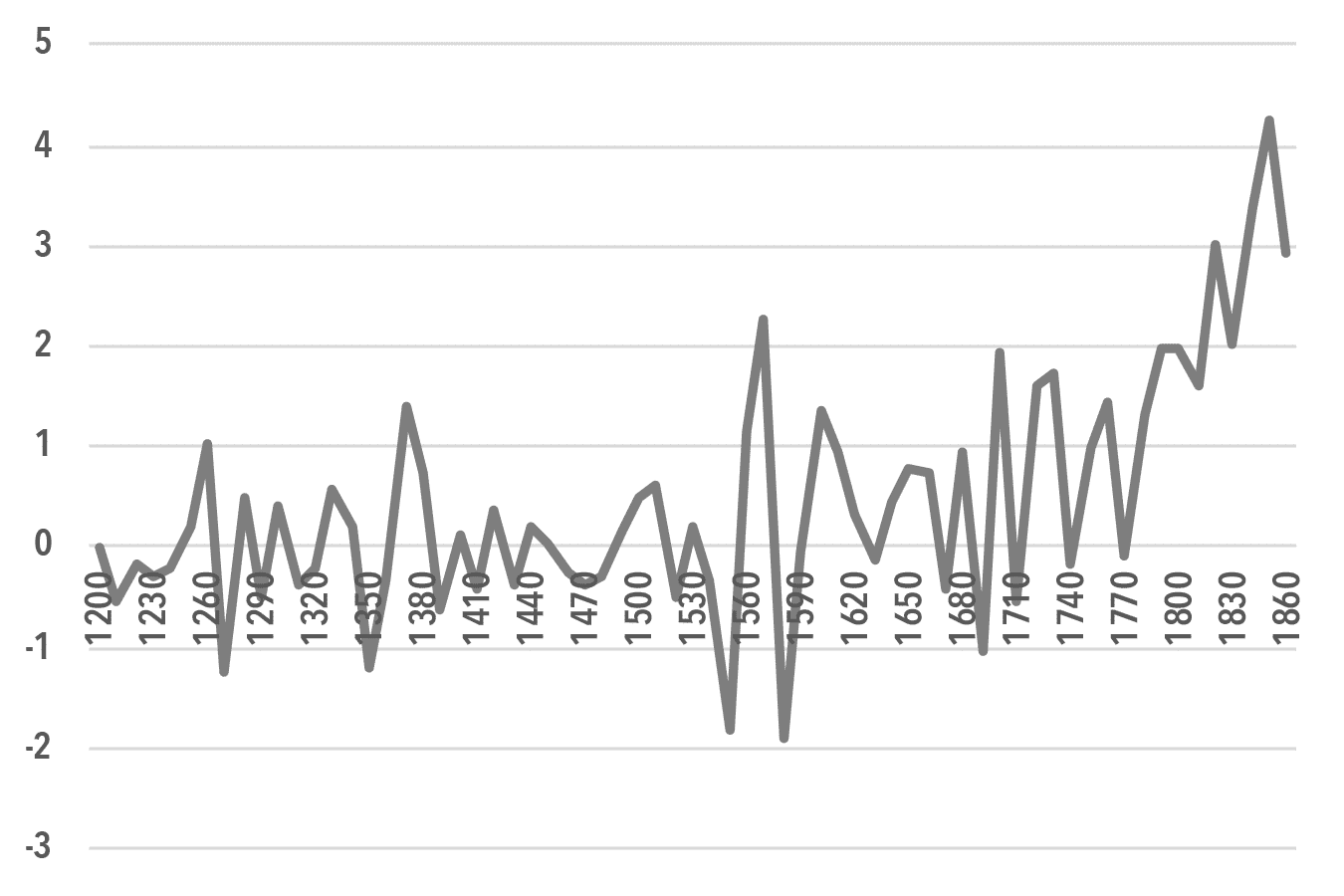

Chart 1 shows the economic surplus as a portion of NNI for England from 1209 to 1868 using Clark’s data. Some argue that feudalism ended in England in the later years of the fifteenth century, whereas others contend that feudalism ended in England in the late eighteenth century or early nineteenth century. As can be seen from Chart 1, the economic surplus as a percentage of NNI declines during the thirteenth and fourteenth centuries and becomes mostly stationary in the fifteenth and sixteenth centuries until it begins to recover in the seventeenth century. In the eighteenth and nineteenth centuries, it then stays at levels not seen since the fourteenth century. According to Clark’s data, total wages grew as a share of NNI as rental and capital income remained mostly the same during the thirteenth to the sixteenth centuries. This wage growth is probably due to the employment growth generated by cities, ports, and increases in “free labor”; labor shortages due to famines and plagues; and the collapse of the demesne system. It is not until the seventeenth century—perhaps due to events such as the continuance of the enclosure movement, the Tenures Abolition Act of 1660, and the growth of large trading companies, colonies, and ports—that capital income begins to rise to higher levels so that the economic surplus as a percentage of NNI comes closer to what it was in the fourteenth century. This increase in capital income could point to capitalism possibly beginning in the seventeenth century.

Chart 1: Economic Surplus/NNI % (1209–1868)

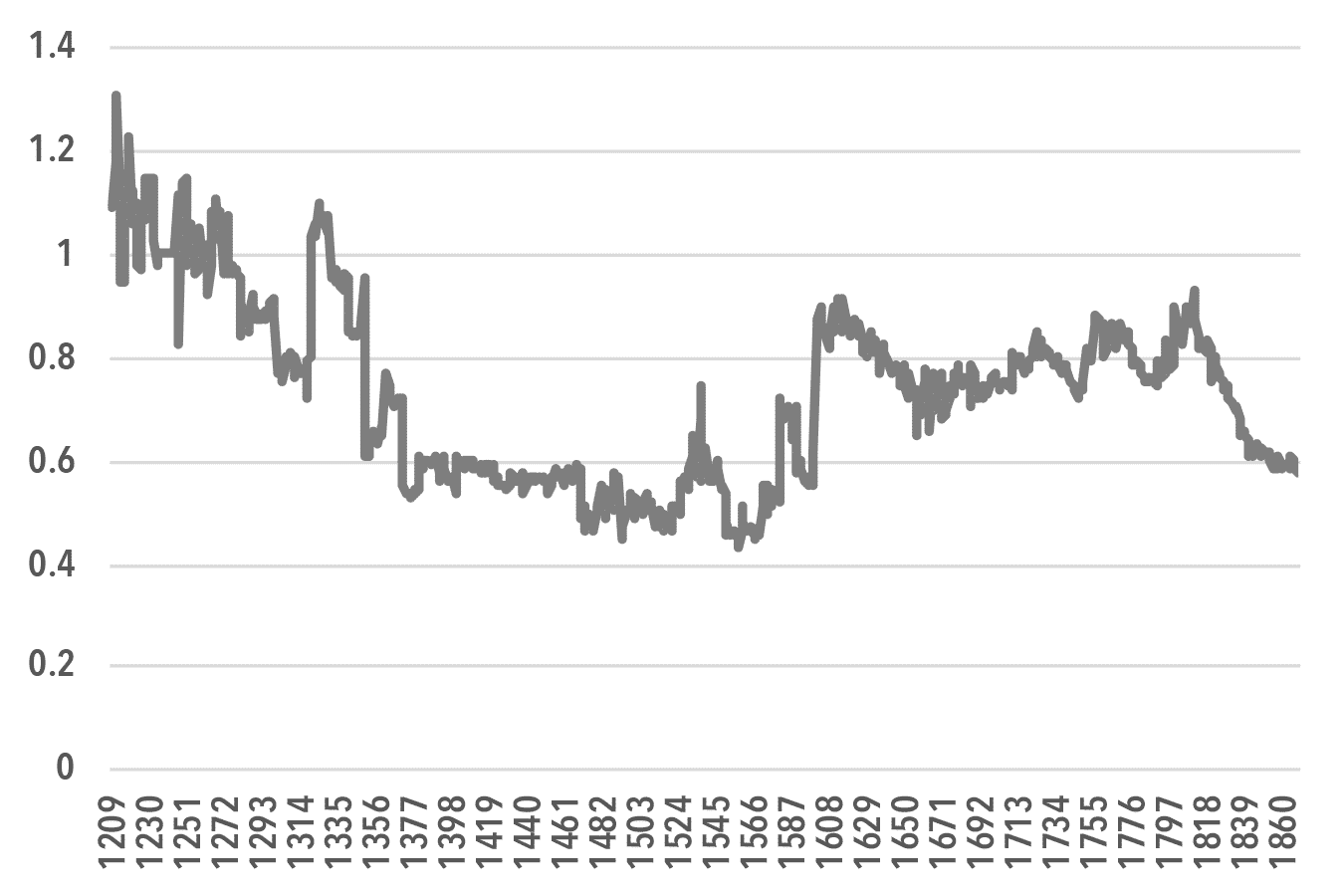

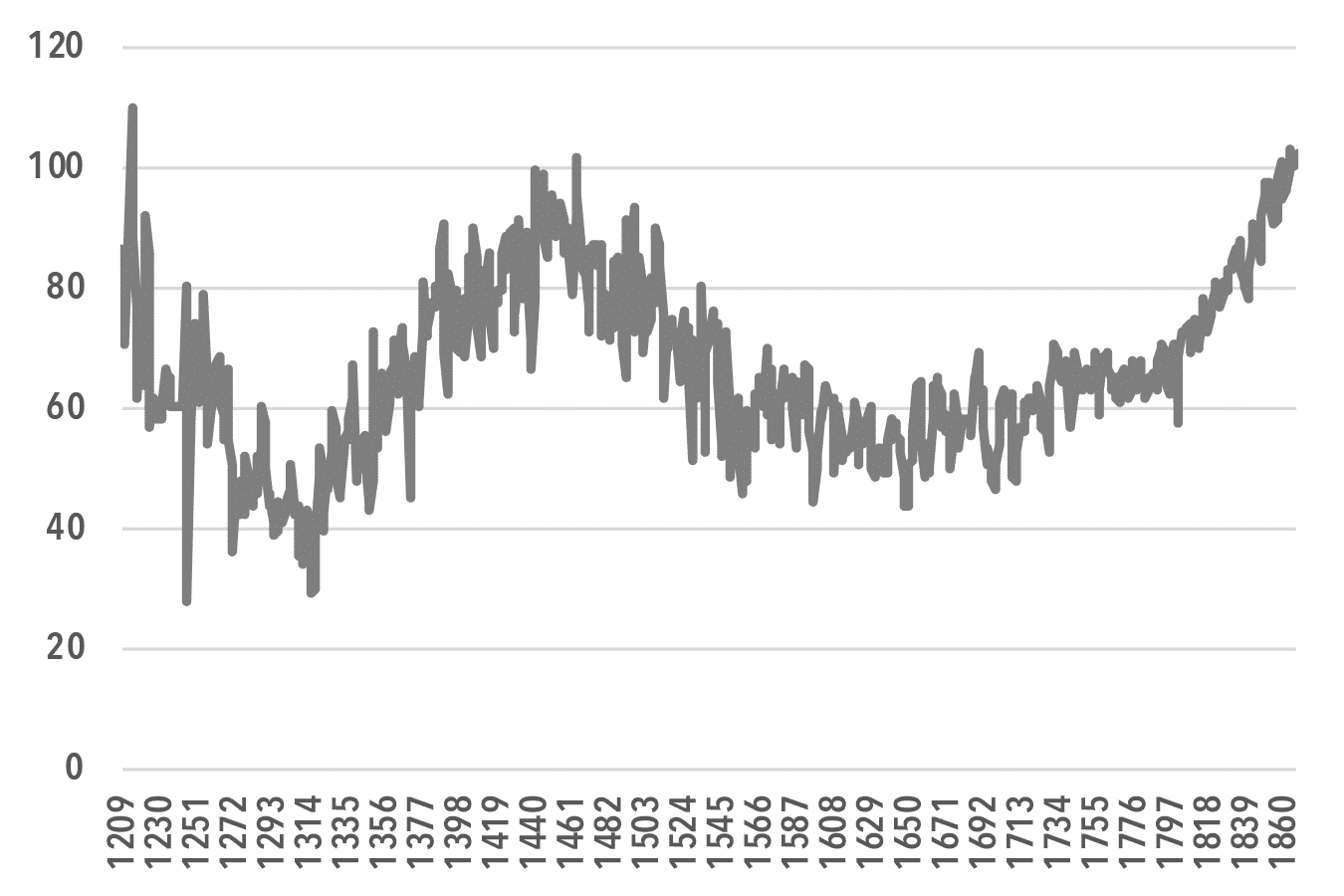

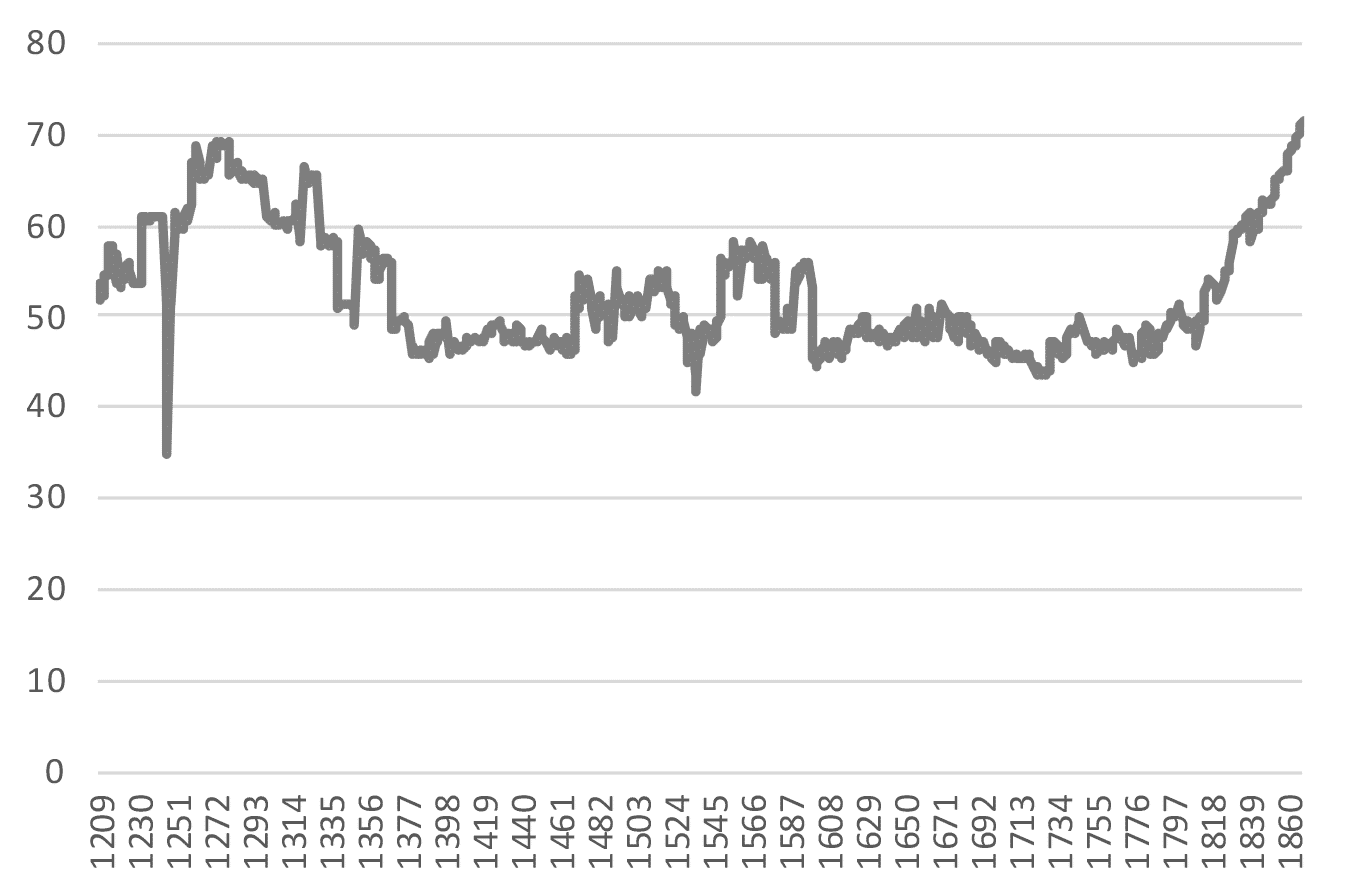

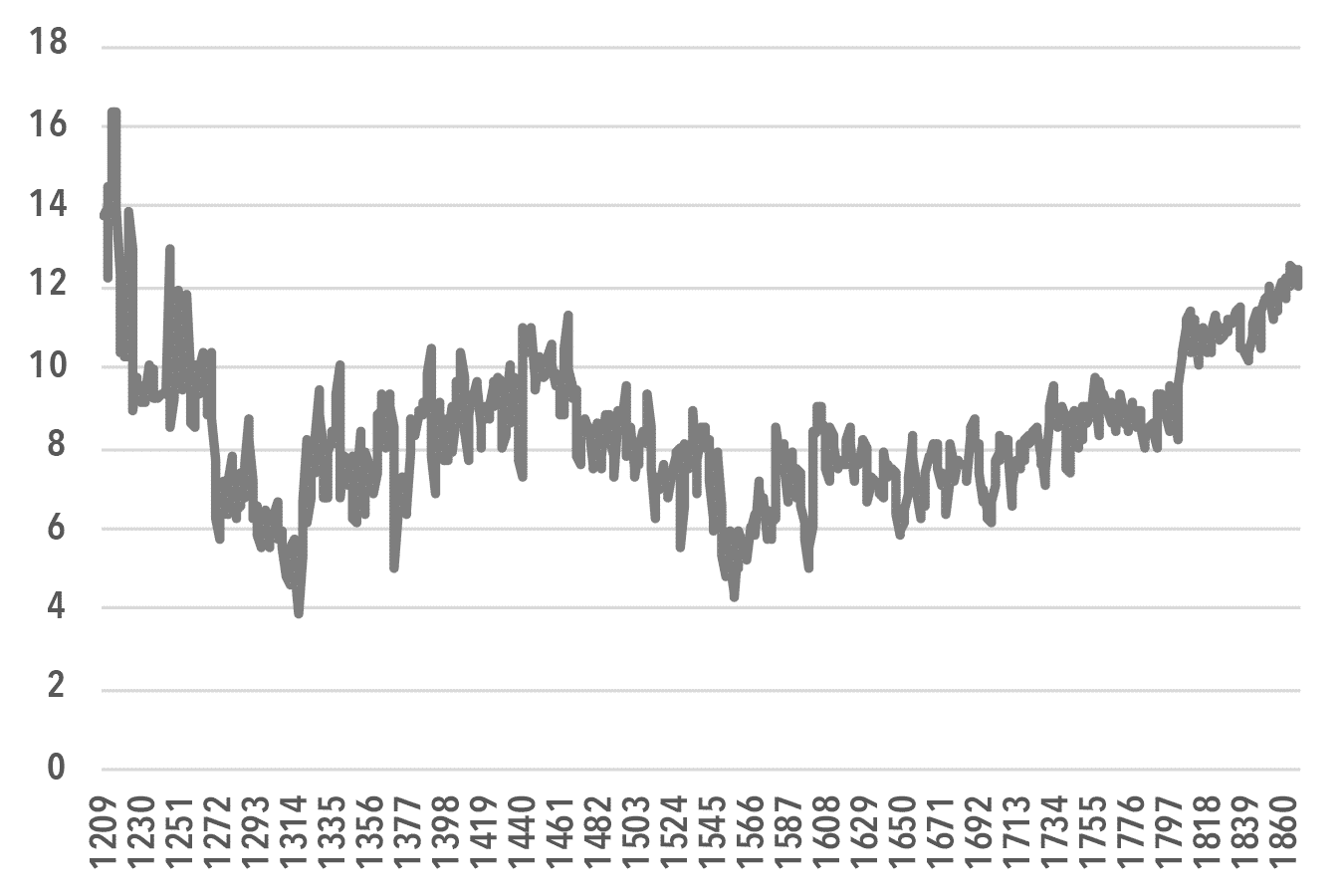

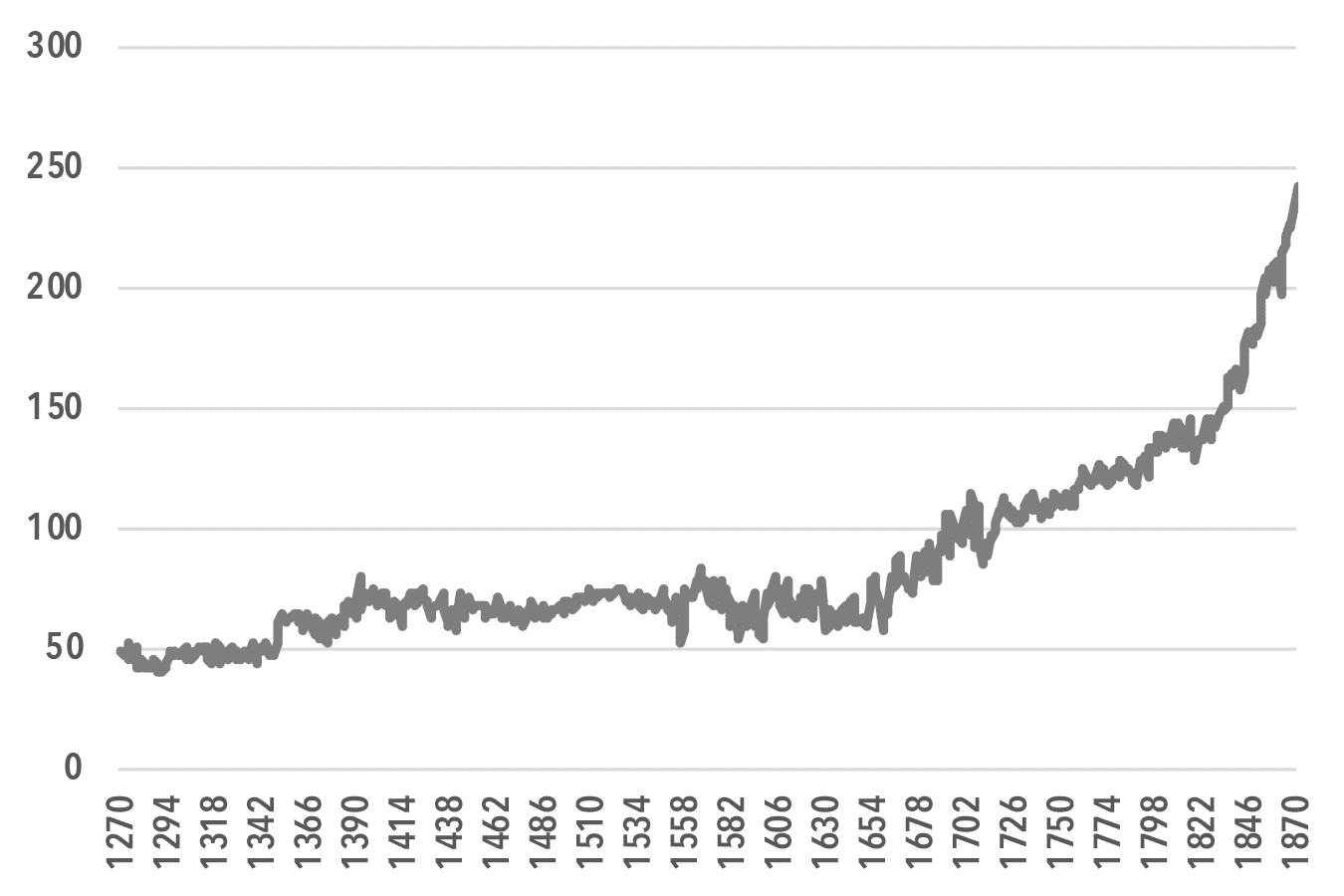

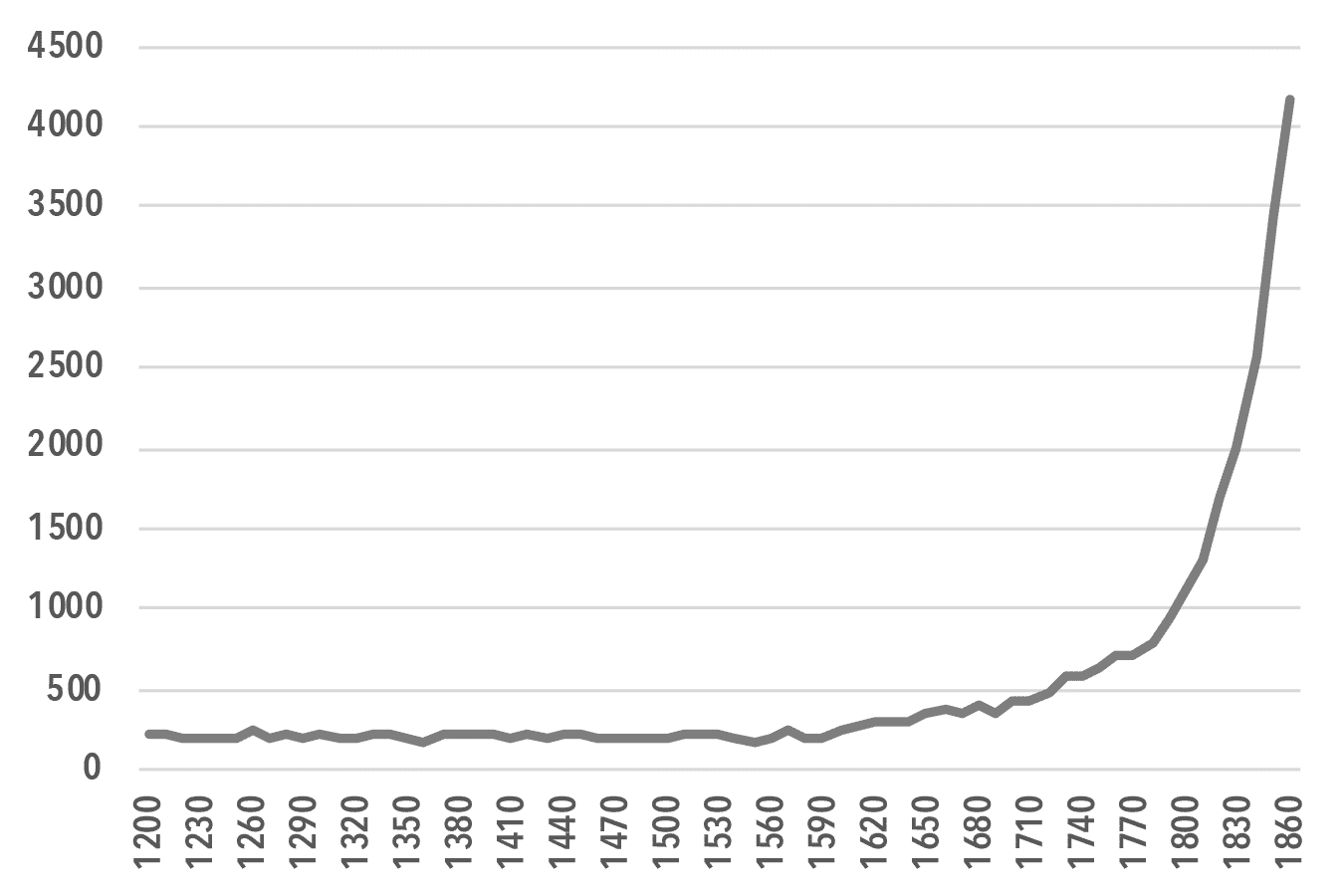

In a pattern similar to that of Chart 1, Chart 2 illustrates the gradual decline of economic surplus relative to wages during the thirteenth and fourteenth centuries, with the exception of the first sixty years or so of the fourteenth century, perhaps due to population and labor force losses due to the Great Famine of 1315–17 and the Black Death, as well as attempts by the nobility to limit wage increases through legislation or taxation.10 Wage income was also a smaller share of economic activity during the thirteenth and fourteenth centuries when compared to subsequent centuries. Economic surplus as a percent of NNI and the ratio of the economic surplus to wages climbed until about the time of the Napoleonic Wars, during and after which they declined through 1868, likely due to wages and labor income becoming a greater share of national income with the Industrial Revolution in England, despite the absolute value of capital income growing. Looking at Chart 3, real NNI per capita (base years of 1860s) declined during the thirteenth century and through the first twenty or so years of the fourteenth century, until it began to rebound and slowly climb back up until the mid–fifteenth century, mostly thanks to the growth of wage income as estimated by Clark. Subsequently, however, real NNI per capita began to decline from the middle of the fifteenth to the sixteenth century, and then held roughly steady until the 1700s. It then began a steady climb upward through 1868, which is about where Clark’s published data stops. Chart 4 plots capital income as a portion of NNI from 1209 to 1868. This chart shows that capital income as a share of NNI basically started to collapse in the fourteenth century and did not really begin to rebound until around the second half of the sixteenth century.

Chart 2: Ratio of Economic Surplus to Wage Income (1209–1868)

Chart 3: Real NNI per Capita (1209–1868, 1860s=100)

Chart 4: Capital Income/NNI % (1209–1868)

Chart 5 shows the ratio of capital to land rent income increasing in the late eighteenth century and climbing dramatically in the nineteenth century. Chart 6 illustrates economic surplus per capita fluctuating in a pattern similar to real NNI per capita shown in Chart 3. It is perhaps the proceeds of capital income earned in the seventeenth, eighteenth, and nineteenth centuries that provided the investment needed to propel England and Britain forward during this period, as shown in the real GDP per capita growth trend in Chart 7, which uses data from Broadberry and colleagues. Finally, Table 1 gives the Pearson correlation coefficients among real GDP per capita, real economic surplus per capita, and real NNI per capita from 1270 to 1868. All coefficients show positive and statistically significant associations among the three variables. Most importantly, as economic surplus rises, so too does GDP per capita and NNI per capita, although the gains in GDP and NNI may not have been equally shared among all classes.

Chart 5: Capital Income/Land Rent Income (1209–1868)

Chart 6: Economic Surplus Per Capita (1209–1868)

Chart 7: Real GDP per Capita (1270–1870, 1700=100)

Table 1: Correlation Matrix for Annual Data

| Real GDP per Capita | Real Econ Surplus per Capita (1860s=100) | Real NNI per Capita (1860s=100) | |

| Real GDP per Capita | 1.000 | ||

| Real Econ Surplus per Capita (1860s=100) | 0.677* | 1.000 | |

| Real NNI per Capita (1860s=100) | 0.527* | 0.855* | 1.000 |

Although Baran claimed that the economic surplus under feudalism should be small when compared to competitive capitalism (seventeenth- and eighteenth-century eras), and even less so when compared to monopolistic capitalism (nineteenth-century era), the charts displayed here may suggest otherwise.11 If Clark’s numbers are correct, then the thirteenth century saw large degrees of economic surplus that dwindled and did not rebound until capitalism became the dominant economic system in the 1700s. This upswing in the 1700s is probably due to the surplus being at least partially reinvested during that time period, rather than being wasted on unproductive activities as in the thirteenth and fourteenth centuries. The high levels of economic surplus for the thirteenth and fourteenth centuries would indicate a much higher degree of wastefulness than what Baran might have estimated and, if Malthus was correct, much of this surplus might have been spent and used to prop up a feudalistic system by spending on unproductive labor and pursuits. With land shortages developing, in turn limiting agricultural production, and with labor force shrinkage due to diseases and famines, then any medieval economic surplus likely began to shrink. Feudalism was plunged into a severe crisis.

The Baran Ratio

Recently, Xu developed the concept of the Baran ratio—an economy’s amount of investment divided by its economic surplus, which Xu defines as a nation’s income share of the 90th percentile and above. However, he uses the share of income of the top 10 percent as an approximation in order to compare different nations.

Ideally, economic surplus could be calculated as the residual of national income deducting social-essential consumption. However, this is often impossible due to lack of data. Alternative methods include utilizing property share of GDP, which equals one minus labor share, and the top income research pioneered by Thomas Piketty. This is particularly helpful when the labor-share data is missing.… I have used the top 10 percent share of the national income as a proxy for surplus. Other top income shares are often not available for most countries in the sample.12

For my purposes, capital, land, and home rental income, as well as indirect tax revenue estimates, are available, so a Baran ratio that uses something close to Baran’s original concept of an economic surplus (capital income + land rental income + home rental income + indirect tax revenue) can be constructed by taking the sum of these and using it as the denominator of a ratio, with the estimated amount of investment in England over time as the numerator, so that:

Baran ratio = Investment / Economic surplus (1)

This basically represents the amount invested out of capital, land, and housing income, as well as public investment. The amount of capital and public investment in England is approximated on a decadal basis from 1200 to 1860 using Clark’s data, which in turn are divided by the economic surplus estimated for each decade. Clark has published real national income, real returns to capital (public and private), capital shares of national income, and capital income estimates on a decadal basis for England from 1200 to 1860. In standard economics and finance textbooks, interest rates, or the returns to capital, are supposed to equal income from capital divided by the value of the capital.

Rate of interest = Income / Capital (2)

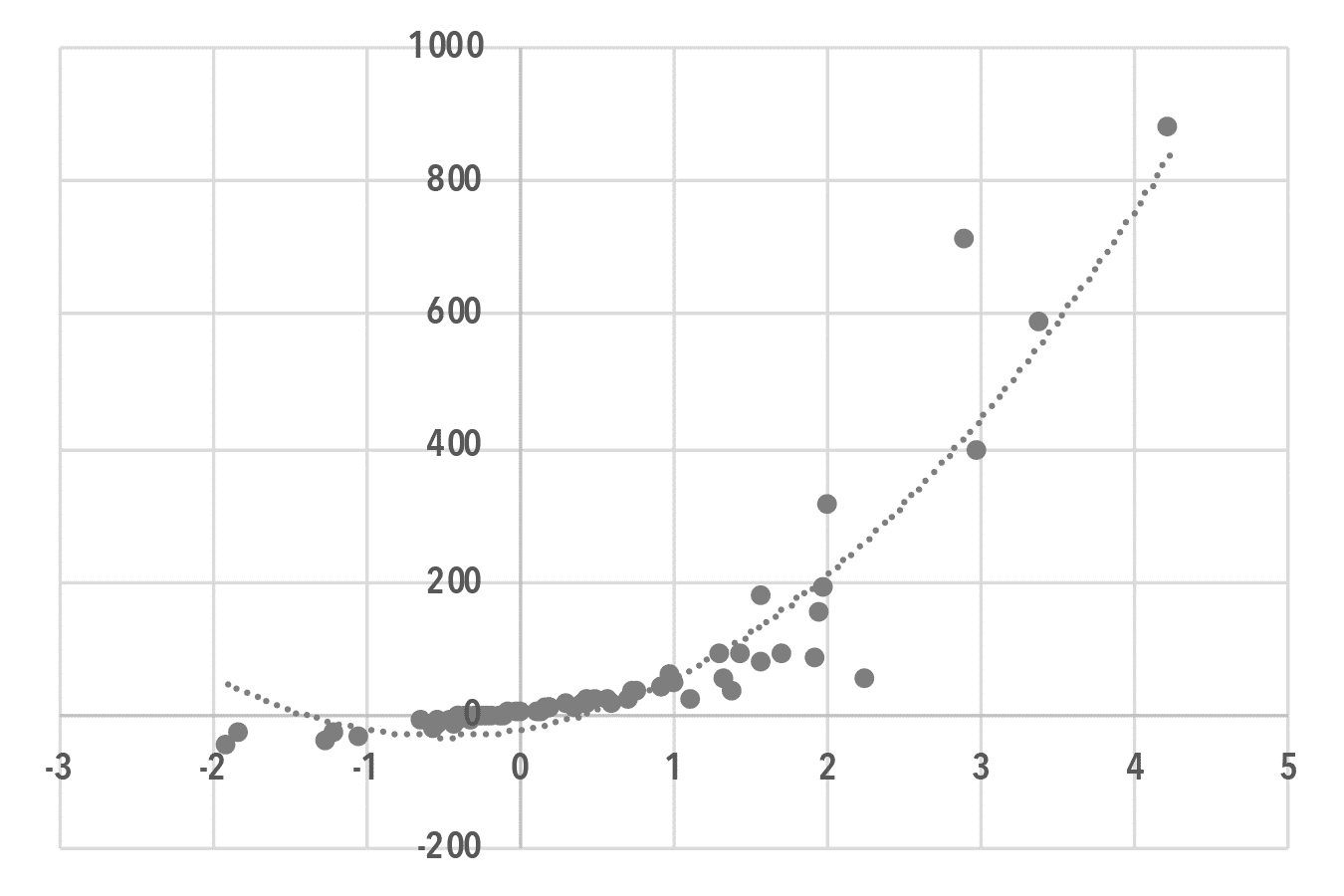

Setting Capital = Income / r , one can estimate the amount of real capital (public and private) in the English economy for each decade from 1200 to 1860 using Clark’s data.13 Chart 8 shows the levels of estimated real capital from 1200 to 1860, which did not really begin to rise until around 1700 or later. When the change in capital levels is calculated from one decade to the next in order to estimate real investment rates from one decade to another, a Baran ratio can be estimated for the decades. Chart 9 shows levels of the Baran ratio from 1200 to 1860, where high levels were not reached on a consistent basis until the late sixteenth century. Levels consistently above 1.0 were not attained until around 1800, likely due to borrowing and using savings or retained earnings to finance investment. When calculating a Pearson correlation coefficient between the Baran ratio and real investment per decade, a statistically significant coefficient of 0.802 is found, indicating a high level of correlation. Table 2 displays this result, showing a statistically significant correlation between real NNI per capita (with the base year of 1860) and the Baran ratio, as well as a statistically significant relationship between real NNI per capita and real investment. Finally, when plotting investment and the Baran ratio, a quadratic relationship is found in Chart 10, where the equation and fit are:

Predicted investment = 39.034 Baran ratio2 + 37.944 Baran ratio – 21.661, adjusted r2 = 0.878, (3)

and both variables are statistically significant at α < 0.05, with Newey-West standard errors.

Chart 8: Real Capital Stock, £ millions (1200–1860)

Chart 9: Baran Ratio (1200–1860)

Table 2: Correlation Matrix for Annual Data

| Baran Ratio | Investment | Real NNI per Capita | |

| Baran Ratio | 1.000 | ||

| Investment | 0.802* | 1.000 | |

| Real NNI per Capita | 0.395* | 0.565* | 1.000 |

Chart 10: Predicting Investment using Baran Ratio (1200–1860)

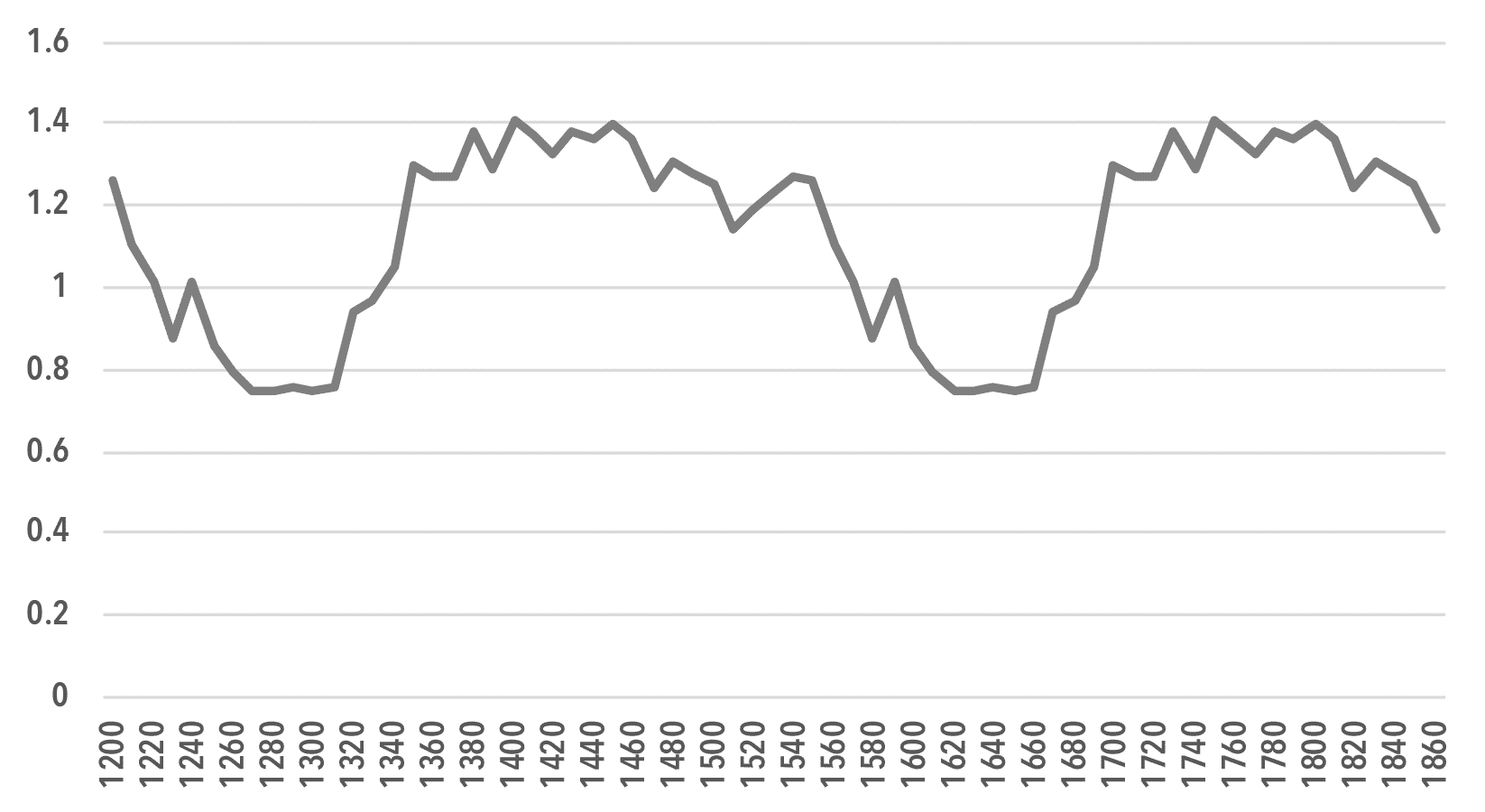

When it comes to productivity levels, mainstream economic theory predicts that greater investment levels in capital should result in greater productivity or greater output per worker. Using Clark’s data, Chart 11 shows that productivity levels for agriculture in thirteenth-century England were fairly high and then fell during the first half of the fourteenth century before rebounding later in that century and in the fifteenth century.14 They then declined during the sixteenth century before returning to higher levels in the seventeenth century, about the time of the English agricultural revolution and the acceleration of the enclosure movement. The Baran ratio depicted in Chart 9 shows consistently higher levels around the 1700s, and Chart 8 does not show higher capital levels until then too. Therefore, the high levels of agricultural to nonagricultural levels of output in the fifteenth and sixteenth centuries have to be explained mostly by factors other than investment, and these may include farmers enjoying greater payments for their output, therefore encouraging them to produce more, or peasants and tenant farmers being coerced to produce more by their landlords and compete against one another, even as the enclosure movement was starting, with more and more peasants having to move off the land.15 The enclosure movement was met with resistance. With the landlords finally triumphant in the seventeenth century, Robert Brenner argues that capital investment in farms would have been safer and more effective, with fewer workers on each farm but greater output per worker.16

Chart 11: Output Per Worker (Ag/Non-Ag) Decadal Basis (1200–1860)

Interestingly, the productivity levels attained in the eighteenth and nineteenth centuries were not dramatically higher than those attained in the peaks of prior time periods. Paul Cockshott cites and uses charts from John McDonald to argue that feudal farms were just as efficient as later forms of farming under capitalism.17 It is only speculation as to whether this was due to coercion and exploitation given a lack of consistent capital investment and innovation prior to the 1600s, or if it was due to low population levels in England during the fourteenth and fifteenth centuries. Chart 6 shows that economic surplus per capita was high during the fourteenth and fifteenth centuries, although the economic surplus as a portion of NNI was low.

Conclusion

The economic surplus in England from the thirteenth up to the eighteenth century does not appear to have been invested in capital to the extent that it would have led to greater levels of economic growth, output, and standards of living in a capitalistic system. Although actually higher in the thirteenth century than what would have been expected, the surplus still dwindled and mostly stagnated for the next several centuries, perhaps due to factors such as plagues, famines, wars, class struggles between serfs and noblemen and then peasant farmers and their landlords, the growth of wage laborers and higher overall real wages, the growth of low-profit-margin tenant farmers, and the proliferation of small but low-profit-margin petty producers who were the forerunners of the competitive stage of capitalism.18 If correct, then this set of factors would support a gradual and evolutionary notion of a transition to capitalism, an economic form that requires the generation of a large amount of surplus and the accumulation and continued reinvestment of at least some, if not all, of the surplus, according to Baran. Cockshott and many others, such as Stephen Resnick and Richard Wolff, have noted that capitalism started in different parts of the globe and suffered many setbacks and failures before fully developing and coming to full dominance as the main economic system in the nineteenth century, and perhaps much of the variation in the charts displayed here illustrate this, as English society transitioned from a mostly feudalistic system to a mostly capitalistic one over several centuries.19 It is also known that feudalism continued to exist as an economic system while capitalism became dominant in England and Western Europe, just as slavery was still an economic form of organization in many parts of the globe by the time of the nineteenth century.

Despite large amounts of surplus in the thirteenth century, and perhaps this was the case in prior centuries too, feudalism did not really practice any form of reinvestment. Therefore, with famine, plagues, and land and labor shortages, the surplus dwindled, setting off a crisis of feudalism, especially for those benefiting from the surplus—the English nobility and aristocracy. With less surplus in the next few centuries, especially relative to wages, the coercion of serfs and peasants could have been one way that a declining economic system tried to get more output and surplus from its workers. This was along the lines of the thinking of Maurice Dobb, Brenner, and others who thought that feudalism ended due to endogenous factors. In the meantime, the growth of cities, ports, foreign trade, town markets, tenant farmers, and wage laborers set in motion the development of institutions that would later help give rise to capitalism as the old feudalistic system died. This kind of analysis was developed by Sweezy and others who argued that mostly exogenous factors caused the downfall of feudalism. A compromise view by Resnick and Wolff claimed that both endogenous and exogenous forces worked together to bring down feudalism and provide a transition to capitalism.

I have used Baran’s concept of an economic surplus to illustrate the crisis that hit feudalism in the fourteenth century and the transition to capitalism, which, if the data displayed here are correct, began to take off in England in the eighteenth century. It does not appear that Malthus’s notion of excessive and extravagant spending by medieval nobility had any long-term benefits for a feudalistic society. Such spending may have improved the employment and utilization of some resources in the short term, but without productive investment, the feudalistic economy was not able to overcome (for example, by investing in new farming or labor techniques) outside shocks such as plagues and famines, or internal contradictions and constraints like class struggle and land and labor shortages. Instead, if Brenner and Dobb are right, coercion of the labor force was relied on to try to keep the feudalistic status quo. However, this failed to yield an economic surplus suitable for keeping the upper class in a strong position in the long run. Instead, a new economic system had to develop that raised the economic surplus back up to its previous levels.

Similarly, capitalism faced a severe crisis on a global basis in the 1930s. The economic surplus collapsed along with the wages and standards of living for millions of workers.20 Some nations resorted to fascism in order to try to restore the economic surplus of their societies to previous levels. Others, such as the United States under Franklin D. Roosevelt’s New Deal, experimented with social and public infrastructure spending in order to keep the capitalistic system from collapsing. John Maynard Keynes argued that, in a capitalistic system, there is a tendency for underinvestment or underconsumption, which can lead to economic crisis.21 He therefore believed that there must be a certain level of socialization of investment or a certain level of government spending on public investment items to keep a capitalistic system from going into periodic crises. In the minds of Baran and Sweezy, this required a certain amount of reinvestment of the economic surplus, whether into productive or unproductive pursuits, although they thought that the Keynesian prescription to remedy economic crises was overly simplistic because capitalism had too many internal contradictions. One problem, according to Baran and Sweezy, was finding enough outlets for any type of productive or unproductive reinvestment of the surplus. Often, there are not enough outlets for such reinvestment, and this in turn could lead to a recession or depression as a decline in investment can lead to a contracting economy.22

If feudalism’s downfall in England was partially or mostly due to its inability to use the economic surplus productively, capitalism’s possible future transition or evolution into another economic system could also hinge on how a society’s economic surplus is used. If the surplus is mostly and continuously used unproductively, similar to feudalism’s wasted expenditures, then capitalism’s future could be in jeopardy. Capitalism’s failure to invest sufficiently in public health and to be prepared for a crisis such as the COVID-19 pandemic is somewhat similar to feudalism’s failures to address famine and disease. The Black Death hit a weak feudalistic system very hard, just as the recent pandemic has hit capitalism. Recognizing and accepting that there are often not enough investment outlets for productive investments, and that there is a growing need for the socialization of investment as noted by Baran and Sweezy, capitalism could eventually start on a transition toward socialism. If the decline of feudalism and its aftermath is any indication, the transition could be a long and continuous struggle.

Notes

- ↩ Long before the Dobb-Sweezy debate, Frederick Engels noted the wastefulness of medieval aristocracies in Europe in 1884. See Friedrich Engels, “The Decline of Feudalism and the Rise of the Bourgeoisie,” Monthly Review 8, no. 12 (April 1957): 445–54; Maurice Dobb, Studies in the Development of Capitalism (New York: International Publishers, 1947); Paul M. Sweezy, “A Critique,” in The Transition from Feudalism to Capitalism, ed. Rodney Hilton (1950; repr. London: New Left Books, 1976), 33–56. Sweezy’s “A Critique” was originally published with Dobb in the spring 1950 issue of Science and Society: Paul M. Sweezy and Maurice Dobb, “The Transition from Feudalism to Capitalism,” Science & Society 14, no. 2 (1950): 134–67. See also Paul A. Baran, “Economic Progress and Economic Surplus,” Science and Society 17, no. 4 (1953): 289–317.

- ↩ Paul A. Baran, The Political Economy of Growth (New York: Monthly Review Press, 1957). In particular, see chapter 2.

- ↩ See also Nicholas Baran and John Bellamy Foster, eds., The Age of Monopoly Capital: The Selected Correspondence of Paul A. Baran and Paul M. Sweezy, 1949–1964 (New York: Monthly Review Press, 2017), 238–39. Both Baran and Sweezy thought that the feudalistic economy was somewhat static and stationary, as well as that, because of wasteful and unproductive activities, any economic surplus generated by such an economy would be small in comparison to that generated by capitalism, which is a more dynamic system with higher levels of productivity and reinvestment of at least part of the economic surplus.

- ↩ Gregory Clark, “The Macroeconomic Aggregates for England, 1209–2008” (Economics Working Paper 09-19, University of California, Davis, 2009).

- ↩ Broadberry, B. Campbell, A. Klein, M. Overton, and B. Van Leeuwen, British Economic Growth, 1270–1870 (Cambridge: Cambridge University Press, 2015).

- ↩ Zhun Xu, “Economic Surplus, the Baran Ratio, and Capital Accumulation,” Monthly Review 70, no. 10 (March 2019).

- ↩ Baran, The Political Economy of Growth; Paul A. Baran and Paul M. Sweezy, Monopoly Capital: An Essay on the American Economic and Social Order (New York: Monthly Review Press, 1966).

- ↩ Baran and Sweezy, Monopoly Capital.

- ↩ Baran, The Political Economy of Growth, 24–25.

- ↩ Lipson, The Economic History of England, vol. 1, The Middle Ages (London: Adam and Charles Black, 1959).

- ↩ Baran, The Political Economy of Growth, 60.

- ↩ Xu, “Economic Surplus, the Baran Ratio, and Capital Accumulation.”

- ↩ Income here is capital income adjusted by Clark’s GDP deflator.

- ↩ This is a result that also surprises Clark.

- ↩ Robert Brenner, “Agrarian Class Structure and Economic Development in Pre-Industrial Europe,” Past & Present 70 (1976): 30–75; Spencer Dimmock, The Origin of Capitalism in England, 1400–1600 (Leiden, Netherlands: Brill, 2014).

- ↩ Brenner, “Agrarian Class Structure and Economic Development in Pre-Industrial Europe.”

- ↩ Paul Cockshott, How the World Works: The Story of Human Labor from Prehistory to the Modern Day (New York: Monthly Review Press, 2019), 95–96; John McDonald, Productive Efficiency in Doomsday England, 1086 (London: Routledge, 2002).

- ↩ Robert C. Allen argues that high real wages in England in the eighteenth century gave yeoman farmers the incentive to innovate and adapt new labor-saving technology and methods. Robert C. Allen, “Why the Industrial Revolution Was British: Commerce, Induced Innovation, and the Scientific Revolution,” Economic History Review 64, no. 2 (2011): 357–84; Robert C. Allen, “The High Wage Economy and the Industrial Revolution,” Economic History Review 68, no. 1 (2015): 1–22.

- ↩ Cockshott, How the World Works; Stephen Resnick and Richard Wolff, “The Theory of Transitional Conjunctures and the Transition from Feudalism to Capitalism in Western Europe,” Review of Radical Political Economics 11, no. 3 (1979): 3–22.

- ↩ Baran and Sweezy, Monopoly Capital.

- ↩ John Maynard Keynes, The General Theory of Employment, Interest and Money (New York: Harcourt, Brace, 1936).

- ↩ Baran and Sweezy, Monopoly Capital.

Comments are closed.